FRTB Implementation: Market Fragmentation and the Critical Role of Data Quality

With the Fundamental Review of the Trading Book (FRTB) implementation date approaching, the market landscape remains divided. Regulatory discussions around transitional multipliers continue and the fundamental challenge for financial institutions has shifted from model selection to data granularity. This article analyses the current market sentiment and outlines why data readiness is the critical success factor for 2026.

Included in this collection:

Open collection

End of support for SAP Bank Analyzer – msg.ORRP as an alternative

Why Europe’s banks need to reassess geopolitical risks

Bundesbank’s Targeted Review of the design of lending guidelines in the LSI environment

AMLR Redefines Risk Analysis: Moving Beyond a Checkbox Exercise – Why Regulators Are Rethinking Their Approach

9th Amendment to the MaRisk 2026: What reliefs does the consultation offer to small and very small institutions (SNCIs)?

Instant Payments Regulation: Implementing Reporting Requirements Efficiently – Excel Upload or an Integrated Reporting Solution?

Preferential Treatment of Retail Exposures in the Credit Risk Standardised Approach (CRSA) – EBA clarifies requirements regarding the granularity criterion

Artificial Intelligence in Treasury – from periodic financial reporting to a continuous management function

Changes to the LSI Stress Test 2026

CRR III and the property business: Removing the brake on new business

The implementation of the Fundamental Review of the Trading Book (FRTB) in the EU is entering a critical phase. The recent ISDA survey from January 12th shows the market is effectively split. Approximately half of the banks (by RWA) advocate for a delay to align with the US timeline while the other half prefers to proceed with the 2027 implementation to ensure planning certainty.

In response to these challenges the European Commission has consulted on a “transitional multiplier”. This mechanism is designed to act as a temporary ceiling, neutralising the capital impact of the new rules for an initial three-year period. Such a measure would provide capital relief, but it risks creating a false sense of security. A multiplier is a temporary regulatory adjustment rather than a structural solution. Institutions that rely solely on this transitional measure without addressing underlying data deficiencies may face significant problems with capital requirements once the multiplier expires in 2029.

The Shift to the Standardised Approach

Regardless of the final timeline, the strategic direction is clear. The introduction of the Output Floor – set at 72.5% of the Standardised Approach (SA) RWA – has fundamentally changed the relevance of the Standardised Approach. It is no longer a fallback or reporting requirement. For many institutions it becomes the binding capital constraint.

Therefore, the operational focus must shift from complex model validation (Internal Model Approach) to ensuring the robustness of the Standardised Approach. As illustrated below, the primary driver of RWA efficiency in the SA is not model sophistication, but data granularity and quality.

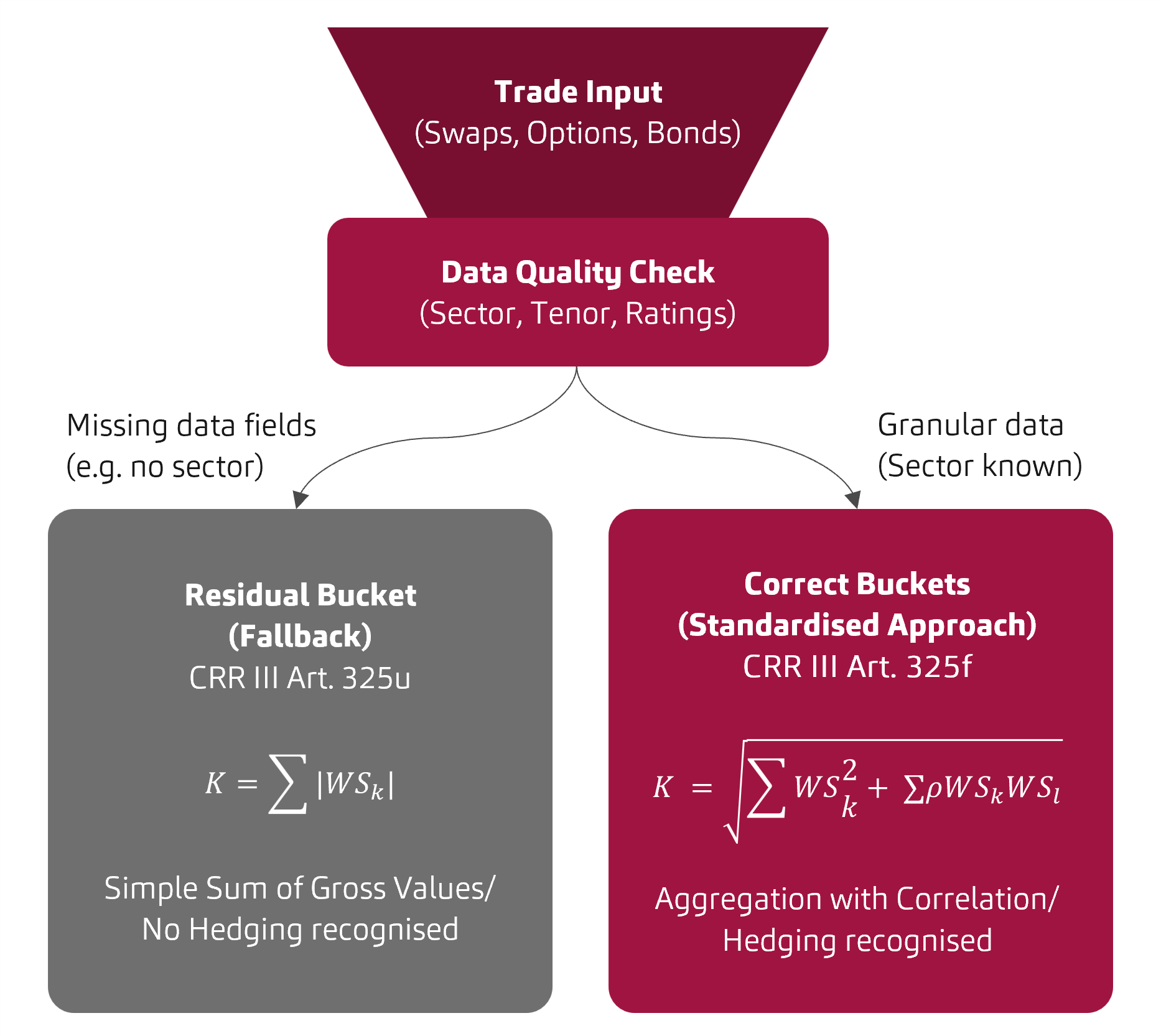

Figure: The mathematical impact of data quality on capital requirements according to CRR III

Operational Challenges in Data Management

Our analysis of ongoing implementation projects identifies three critical data-driven challenges that directly impact capital consumption:

1. The Granularity of Sensitivities (Bucketing Risk)

As shown in the illustration above, the Sensitivities-based Method (SbM) relies heavily on correct bucketing.

- Mechanics: Trades allocated to correct buckets benefit from correlation, allowing long and short positions to offset each other (see CRR Art. 325f).

- Risk: If legacy systems fail to produce granular sensitivities (e.g. missing sector codes) trades fall into the “Residual Bucket” (see CRR Art. 325u). Here, the regulator enforces a simple sum of gross values, i.e. effectively eliminating hedging benefits and drastically increasing RWA.

2. The "Look-Through" Requirement for Funds

Banks and asset managers holding Collective Investment Undertakings (CIU) face strict “look-through” requirements (see CRR Art. 325j).

- Challenge: Incomplete data feeds often fail to capture all underlying ISINs.

- Impact: Without a look-through, institutions are forced to apply punitive fallback risk weights (often treated as “other sector” or “unrated”). This treats a diversified fund effectively as a high-risk equity position. Ensuring complete and granular data feeds for funds is therefore a high-priority lever for RWA optimisation.

3. Residual Risk Add-On (RRAO) Classifications

The Residual Risk Add-On (RRAO) is a capital surcharge intended for exotic instruments.

- Challenge: In many legacy booking systems trade flags for complexity are outdated. Vanilla products such as standard swaps are frequently misclassified as complex due to historical system migrations.

- Impact: Incorrect RRAO flagging attracts a flat 1% capital charge on the notional amount. For large derivative portfolios misclassification leads to a substantial and unnecessary increase in capital requirements.

Conclusion

The political debate regarding implementation dates and multipliers did not yet finish. However, institutions should utilise their time and resources to conduct comprehensive data readiness assessments. By addressing data gaps in look-through capabilities, correcting legacy trade classifications and ensuring granular sensitivities mapping, banks can structurally reduce their RWA consumption.

Optimising Regulatory Implementation with msg for banking

As experts in regulatory reporting and financial risk management, msg for banking supports institutions in navigating the complexities of CRR III. Our approach combines deep regulatory expertise with technical implementation skills to ensure efficient RWA calculation and robust data management.

Contact us to discuss how we can support your FRTB data strategy and capital optimisation.

Sources

-

1. Regulation (EU) 2024/1623 of the European Parliament and of the Council (CRR III), 31 May 2024

-

2. European Commission, Targeted consultation on the application of the market risk prudential framework, April 2025

-

3. Commission Delegated Regulation (EU) 2025/1496 amending Regulation (EU) No 575/2013 as regards the date of application of the own funds requirements for market risk, 12 June 2025