Wero 2025/2026 – The European payment engine is picking up speed

News, developments and strategic significance for banks, PSPs and acceptance points

What are the important developments at the European Payments Initiative (EPI) and Wero from the perspective of merchants, service providers, businesses, authorities, associations and other acceptance points, as well as payment service providers and banks? A comprehensive overview.

- Introduction

- Additional channels and technological developments

- Significance for acceptance points

- Wero is growing in Europe: Where the payment standard has already arrived and who is following suit

- Wero in a strategic context

- Impact on banks, issuers, PSPs and acquirers

- Conclusions and recommendations for acceptance points

- Conclusion – Wero is at a decisive threshold

- Sources

Included in this collection:

Open collection

E-Invoice 2026+: A requirement for businesses – a strategic opportunity for banks and payment service providers

SEK, DKK, NOK: How ISO 20022 connects Nordic payments to your ERP

The Digital Euro versus Consumer Payments – an unnecessary controversy

Beyond Borders – Corporate Survey Results Unpacked

Instant Payments Regulation: Implementing Reporting Requirements Efficiently – Excel Upload or an Integrated Reporting Solution?

Another step toward implementation: The ECB’s digital euro pilot program launches

FiDA and Open Finance: When data becomes a competitive advantage

DTAZV will be phased out in November 2026 – here's what Corporates and SAP Customers need to prepare for now

The digital euro in everyday payments

Wero 2025/2026 – The European payment engine is picking up speed

Introduction

The European payment solution Wero, launched in 2024 as a mobile peer-to-peer (P2P) service, made significant technological and market progress in 2025: following its launch for small business payments, the first e-commerce acceptance points in Germany, France and Belgium followed starting in November 2025. In 2026, Wero is also set to be available at the point of sale (POS), thus covering almost all retail use cases.

The account-to-account (A2A) service is currently live in Germany, France and Belgium. The rollout is currently taking place in the Netherlands and Luxembourg. At the same time, the European Payments Initiative (EPI) is open to cooperation with European payment systems, which gives the solution additional significance in the geopolitical context. Against the backdrop of growing transatlantic tensions, Wero, as a purely European and cross-border solution, is becoming increasingly strategic for the economy and finance in the EU.

However, despite visible progress, it remains to be seen whether Wero can prevail over established providers such as PayPal, Apple Pay, Google Pay, Amazon Pay and Alipay, as well as credit card schemes. In the course of this article we explain why it makes commercial sense for merchants to offer Wero and related payment services to customers at the earliest opportunity.

Additional channels and technological developments

Easy payments for small businesses and associations

The introduction of Wero continues to progress in the countries already participating. When it was launched in 2024, only P2P payments were possible, comparable to the former Kwitt system used by savings banks in Germany.

In 2025, P2PRO (person-to-professional) was added. It enables small businesses (craftsmen, market stalls, associations, taxi and transport services, etc.) and their customers to make account-to-account payments very easily via a QR code. This does not require a third party, but is based solely on the existing bank details of both parties. The merchant pays a fee of around 0.7% of the transaction amount.

Rollout in e-commerce and in-store retail in Wero countries

Acceptance in e-commerce was launched among German online retailers in November 2025 and in France and Belgium in January 2026. Numerous large retailers accept the new European payment solution, enabling their customers to make fast, low-cost, account-to-account payments. The rollout in in-store retail is scheduled to begin at the end of the year. In the future, Wero is also expected to support additional functions, such as recurring payments including subscription management, buy-now-pay-later (BNPL, instalment payments and purchase on account) and bonus programmes for customer loyalty.

Significance for acceptance points

Wero opens up special potential for retailers, service providers, businesses, associations, public authorities and other acceptance points. Here we provide a comparison with international card schemes and wallet solutions based on individual features.

Costs: Transaction costs are lower with Wero (approx. 0.7% of turnover) than with international card schemes such as Visa and Mastercard (approx. 1-3%) or wallets such as PayPal (approx. 2.5-3.5%). It should be noted that mobile channels, such as Apple Pay, may add a top-up of around 0.5-1.0%.

Real-time payment receipt, higher liquidity: Wero uses SEPA Instant Payment or – in the case of interoperability with existing national payment services – other instant rails of the participating countries. This means that the payment recipient has access to the funds within 10 seconds of the payment being triggered – unlike with international schemes, where the payment flow takes ‘detours’ and only reaches the business account after a delay.

No additional contractual relationship, simplified verification process: With Wero, there are no intermediary service providers. A merchant who already has a business account with a bank and accepts digital payments therefore does not need any additional contractual relationships. This eliminates the need for additional verification under the Money Laundering Act (KYC = Know Your Customer). The bank or PSP only needs to extend the service to include Wero acceptance.

Direct account-to-account processing: Unlike other international providers such as Mastercard, Visa, PayPal or Amazon Pay, payments with Wero are processed directly from account to account. As European banks and financial institutions have joined forces for this purpose, the payment process takes place without any intermediate steps or the involvement of intermediaries.

Data remains with the merchant: Because Wero does not use intermediaries, no data flows out of the merchant-bank or merchant-customer relationship. Under EU rules, banks are also not allowed to use this data for non-business purposes.

Compliance with EU regulations: Wero meets all legal and regulatory requirements of the EU and participating countries. This is a significant advantage over non-European payment methods for authorities and regulated industries such as the insurance industry.

Cross-border: With a connection to Wero, customers from several EU countries can be served in future. This puts Wero and the payment services connected via interoperability in a better position than methods with national coverage, but not worldwide, such as the global methods of credit card schemes and wallet solutions.

Representation of merchant interests in buyer protection: In the event of problems such as chargeback claims that are not mutually agreed upon by the merchant and the customer, a dispute can be opened via the banking or Wero app. Both the buyer and the merchant can upload documents as evidence to support their position. The final decision on the outcome of the dispute is then made by the banks, meaning that no third-party providers such as PayPal, with their own business interests, are involved in this process.

A payment method for e-commerce and in-store retail: Similar to credit cards, Wero can be used in both channels in the future – a significant advantage over national methods such as girocard (DE) and iDEAL (NL). Wero is not conceptually suitable for MOTO (mail order/telephone order) in the traditional sense, but re-routing in e-commerce or Paylink provides a modern approach.

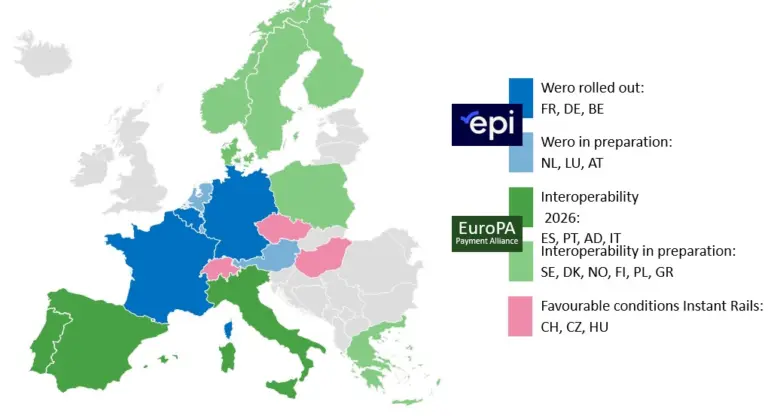

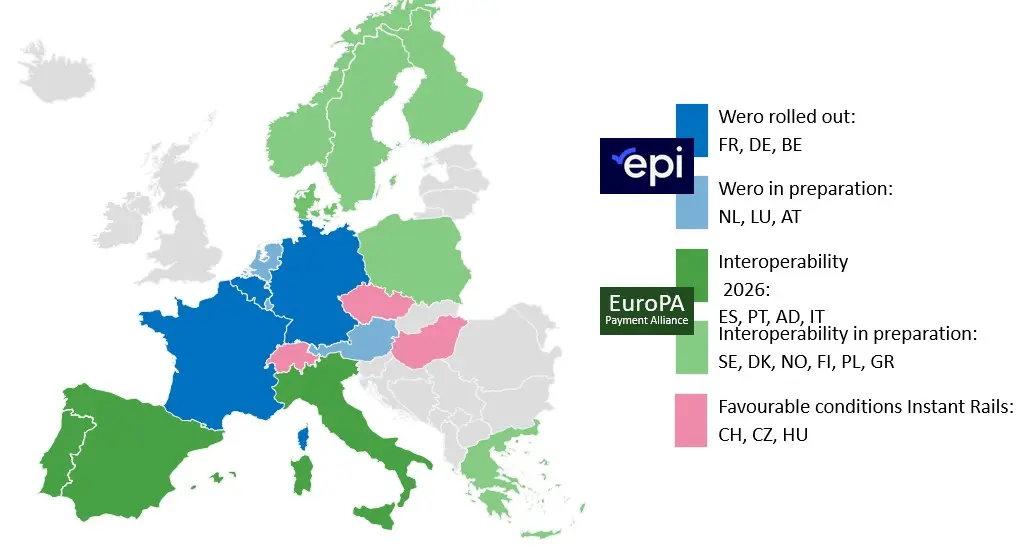

Wero is growing in Europe: Where the payment standard has already arrived and who is following suit

Wero is increasingly developing into a pan-European payment infrastructure whose reach extends far beyond the initial launch countries. While Germany, France and Belgium were the first markets to go live and have already seen widespread rollouts in banking apps and merchant networks, a growing network of other countries is forming around Wero, which are either about to join or will participate via national systems that are expected to be interoperable. EPI plans to cover 16 countries in Europe1.

Market penetration on the payer side

The potential reach among end customers in the participating countries has now risen to a remarkable level of nearly 90%. This refers to those current accounts for end customers that are already actively used for Wero or are ready for use.

| Major banks and banking groups | Wero-compatible accounts/total current accounts | Market coverage (potential reach) | |

| Germany | Sparkassen, VR-Banken, Postbank, Deutsche Bank, ING Bank; Teilnahme angekündigt: Commerzbank, N26 | 124 Mio./140 – 150 Mio. | ≈ 84 % |

| France | Crédit Mutuel Group (inkl. CIC), Groupe BPCE, BNP Paribas Group, Société Générale Group, La Banque Postale | 110 – 115 Mio./120 – 130 Mio. | ≈ 90 % |

| Belgium | BNP Paribas Fortis Group, KBC Group (KBC / CBC), Belfius, ING Belgium | 16 – 18 Mio./18 – 20 Mio. | ≈ 90 % |

| Netherlands | ING Bank, Rabobank, ABN AMRO Bank | 26 – 29 Mio./30 – 32 Mio. | ≈ 90 % |

| Luxembourg | Spuerkeess (BCEE), BGL BNP Paribas, BIL, Banque Raiffeisen, POST Finance | 870 – 990 Tsd./950 – 1.050 Tsd. | ≈ 90 % |

| Austria* | Raiffeisen Bank International (RBI); Issuing PSP: PSA Payments Service Austria | N.N. | N.N. |

*) Specific rollouts by individual banks and therefore reliable coverage figures are not yet available for Austria.

Germany: Circle of participating banks grows

Wero has gained considerable momentum in Germany. Since its launch in 2024, Postbank, Sparkasse and VR Banks have come on board, with Revolut, ING and Deutsche Bank joining in 2025. At the end of 2025 N26 announced its participation2 – a sign that the European payment system is becoming increasingly attractive to digital players. Particular attention was drawn by Commerzbank, the country’s second-largest retail bank, when its CEO Bettina Orlopp officially announced the participation at the press conference on the annual results on 11 February 2026³ – after the bank had withdrawn from EPI in 2022 as a founding member, this marked a clear U-turn and a strong commitment to the European alternative to PayPal, Apple Pay, and others.

With the growing circle of large institutions, momentum is building that could give Wero real breadth in the German market for the first time. The question now remains whether retailers and customers will follow suit at the same pace. Among the first to accept Wero in e-commerce in Germany are Lidl, Rossmann, Decathlon, Hornbach, Eventim, DPD, Zooplus, CEWE and Cineplex.

France: High reach in P2P – e-commerce as the next step in scaling

In France, Wero has been available nationwide since the second half of 2024 and has been able to build on very high bank coverage from the outset. The major French banking groups integrated Wero into their banking apps at an early stage, enabling the service to quickly establish itself as the successor to Paylib. Usage in the P2P environment developed accordingly strongly: within the first year, approximately EUR 7.5 billion was transferred by 43 million registered users at Wero across Europe, with a significant portion of this attributable to the French market.4

On this basis, EPI is now preparing the transition towards merchant acceptance. Following initial P2PRO scenarios involving QR code-based payments, Wero will be rolled out on a broad scale in e-commerce in France in 2026. Several major merchants and service providers are among the acceptance points, including Air France, E. Leclerc, ESF, Orange/Sosh, Veepee and Dott5. In addition, the Direction Générale des Finances Publiques (DGFIP) plans to use Wero in public institutions (museums, hospitals, etc.), which gives the process special regulatory and institutional significance. 6 France is thus evolving from a mature P2P market into a key market for the scaling of Wero in e-commerce and serves as a reference for EPI for further European expansion.

Belgium and Luxembourg: Migration of established Payconiq markets to the Wero ecosystem

In Belgium and Luxembourg, Wero is building on the long-standing use of Payconiq and Bancontact, where P2P payments, P2PRO use cases in small businesses and QR-based payments at the POS are already widely established. Wero has been live in the P2P environment since the end of 2024 and will gradually take over existing merchant acceptance under a joint Bancontact and Wero platform (Belgium)7 and the Payconiq migration (Luxembourg)8 from 2026 onwards. The planned e-commerce rollout from 2026 onwards is intended to scale this nationally grown acceptance to a pan-European level for the first time. Both countries are thus developing into reference markets for the replacement of established national payment systems by Wero – at a rapid pace and without any structural disruption for merchants and users.

Netherlands: Wero grows overnight – thanks to iDEAL

The Netherlands has iDEAL, one of the strongest A2A payment systems in Europe, for e-commerce. It was introduced in 2005 and covers over 90% of current accounts for private customers on the end customer side. More than 70% of e-commerce sales are made via iDEAL.

With the takeover of iDEAL by EPI in 2023, Wero gained immediate access to the Dutch mass market. In the Netherlands, iDEAL | Wero is now used by around 210,000 to 350,000 acceptance points9 and covers around 72% of all e-commerce payments.10 This reach is supported by major retail banks such as ING, Rabobank and ABN AMRO, supplemented by almost the entire rest of the country’s banking landscape.

The integration into Wero, which has been ongoing since 1 January 2026, enables merchants to reach the established user base without any technical changes. For Wero, this means a surge in acceptance practically overnight – combined with lower costs for merchants and a noticeable strengthening of European payment alternatives.

Austria: Preparations for participation are underway

In Austria, Raiffeisen Bank International has been an official member of EPI since 26 November 2025.11 They have been connected as an Acceptor PSP since the end of 2025 and will enable merchants to accept payments in e-commerce from the beginning of 2026. An expansion to brick-and-mortar retail is planned for the future, but no date has been set. At the same time, Payment Services Austria (PSA) has been preparing issuing support for Austrian and German banks since January 2026.12 No specific start dates for the issuance of Wero to end customers have been announced yet.

The significance of this growing country landscape

What makes regional distribution particularly relevant:

- Network effect: Merchants gain access to pan-European customer flows with a single payment standard;

- Cost advantages: A2A payments reduce dependence on non-European card and wallet schemes;

- Regulatory connectivity: The EU actively promotes instant payments and digital sovereignty – Wero fits perfectly into this agenda;

- Technological flexibility: National systems do not have to be abolished, but can be connected via interoperability;

- Gain in sovereignty: The more countries participate, the stronger the European counterweight to US and big tech-dominated payment structures becomes.

Wero in a strategic context

Europe’s response to US payment dominance

With Wero, the EPI is pursuing the goal of a European, sovereign payment alternative in order to reduce dependence on US and Asian providers.

The challenges are clear:

- the strong market position of PayPal, Visa, Mastercard, Apple Pay, Google Pay and Amazon Pay, as well as the upcoming services Alipay and WePay;

- geopolitical risks (control structures of non-EU companies);

- and a historical lack of European payment sovereignty.

EPI itself describes the e-commerce launch of Wero as a decisive step towards a common European payment system that banks, PSPs and merchants are jointly promoting.

Alliance of European A2A payment providers EuroPA + EPI

In a Memorandum of Understanding (MoU)13, EPI and other European payment services declare their joint intention to establish a sovereign, pan-European payment system based on existing European payment solutions. The cooperation follows the collaboration announced in June. At the heart of the agreement is the interconnectivity of existing payment solutions from EPI and members of the EuroPA Alliance via a central technical hub based on European standards and European infrastructure. This hub is intended to create the basis for daily, instant cross-border payments.14 This step has been expressly welcomed in merchant media.15

| Service | Country | Interoperability |

| Bizum | Spain, Andorra | from 2026 |

| Bancomat | Italy | from 2026 |

| MB Way (SIBS) | Portugal | from 2026 |

| Blik | Poland | in preparation |

| IRIS | Greece | in preparation |

| Vipps | Norway | in preparation |

| MobilePay | Denmark, Finland | in preparation |

| Vipps/Swish | Sweden | in preparation |

The target system should enable over 130 million users of the participating solutions to

- send and receive money between private individuals (P2P) across borders and

- make payments in e-commerce (from 2026) and at the POS (from 2027).

Consumers and merchants will be able to continue using their familiar national solutions and services, but now with extended European reach. The system will be based on existing European standards, in particular instant account-to-account payments, supplemented by additional technical connections.

In the first phase of expansion, the initiative will cover 14 European markets: Andorra, Belgium, Denmark, Germany, Finland, France, Italy, Luxembourg, the Netherlands, Norway, Austria, Portugal, Spain and Sweden. This increases the reach of all participating services (including Wero) to approximately 84% of the population of the EU, Norway and Andorra. Other countries can join at any time, further strengthening the reach.

Prospective integration via Instant Rails

Non-euro countries could also become part of the Wero ecosystem in the long term, provided that the regulatory conditions are in place. These include Switzerland, Czechia and Hungary due to their high affinity for instant payments. Participation would be more realistic through interoperability than through full Wero implementation. As these countries are members of the SEPA zone, payments can be made as SEPA Instant Payment.

Figure 1: The ongoing expansion of interconnected European A2A payment methods

EPI calls on ECB to join forces

In November 2025, the EPI sent an unusually strongly worded letter to leading European decision-makers.16 In it, Director Martina Weimert clearly criticises the ECB’s ‘Digital Euro’ project. She warned that the project had been designed without a clear strategic framework and would lead to duplication of structures and unnecessary inefficiencies – especially since Europe already had a functioning real-time payment infrastructure in the form of instant payments.

In addition, the Digital Euro addresses precisely those usage scenarios that private providers such as Wero currently serve. Instead of reducing the market share of international players such as PayPal, Apple Pay and Alipay, the ECB project could even open up additional growth opportunities for them.

In the letter, Weimert also raises the fundamental question of the role of the state in payment transactions. Private-sector solutions have a clear advantage in terms of cost structure, market proximity and speed of innovation, she says. Her call for Europe’s banks to join forces and develop a common strategic line to secure the continent’s digital sovereignty in payment transactions is unambiguous.

Impact on banks, issuers, PSPs and acquirers

The introduction of Wero and the increasing prevalence of European A2A payment methods are fundamentally changing roles and business models in the payments industry. For banks, payment service providers and acquirers, this presents new strategic opportunities, but also requires operational adjustments. The following points provide a structured overview of the most important impacts on the various market participants.

For banks/issuers

- Assumption of a new role as providers of an independent European payment solution.

- Opportunity to reduce costs associated with card and scheme fees.

- Strengthening of the customer interface through integration into existing banking apps.

- Improvement of their own competitive position vis-à-vis non-banks and international payment providers.

For PSPs and acquirers

- Development of new business models in the A2A environment.

- More attractive positioning within the European payment market.

- Expanded connection options for merchants – initially in e-commerce, and in the future also at the point of sale (POS).

Conclusions and recommendations for acceptance points

If you accept or intend to accept payments via one or more payment methods in retail, services, public authorities, associations or elsewhere, these conclusions are obvious:

- Wero and cooperating methods (hereinafter referred to as ‘Wero & Co’) offer you advantages over other payment methods in most cases.

- As a rule, there is no disadvantage in offering Wero & Co alongside other payment methods.

- If you do not yet offer Wero & Co, you can have your bank and PSP set up acceptance as soon as it becomes available.

- The more customers use Wero & Co, the greater the advantages for you.

- As the above advantages usually apply to you as well, you should be keen to encourage your customers to use Wero & Co. Incentives such as discounts or bonus points would be suitable for this purpose, while at the same time complying with the surcharge ban under PSD3/PSR.17

Conclusion – Wero is at a decisive threshold

Wero is on its way to establishing itself as a European alternative to credit card schemes, PayPal, Amazon Pay, Apple Pay, Alipay, etc. The expansion of functions, broad merchant acceptance, technical maturity and integration into government digital initiatives are giving the project momentum.

However, the political escalation surrounding the Digital Euro shows that Wero is no longer just a niche product, but part of a strategic course for the future of European payments.

Whether Wero will prevail in the long term depends largely on:

- its appeal to end users,

- its cost-effectiveness for merchants,

- the consistency of banks in Europe,

- cooperation with existing national payment services in Europe, and

- regulation and competition from the digital euro.

But the path is clear: Europe has the opportunity to rebuild its sovereignty in payment transactions – and Wero & Co are the central building blocks for this.

Sources

-

1. EuroPA and EPI Join Forces to Deliver Instant Pan-European Payments Across 15 Countries, Europawire, 24.6.2025

-

2. N26 schließt sich dem europäischen digitalen Zahlungssystem Wero an, N26, 04.12.2025

-

3. Warum die Commerzbank nun doch bei Wero mitmacht, Handelsblatt, 11.02.2026

-

4. Wero prépare son déploiement dans l’e-commerce, Treds-Tendances, 16.09.2025

-

5. Wero s’attaque au commerce en ligne” Revue Banque, 16.09.2025

-

6. Après le paiement entre particuliers, Wero permet de régler ses achats en ligne, Le Figaro, 16.09.2025

-

7. Payconiq is disappearing – but nothing changes for you thanks to Wero and Bancontact, BNP Paribas Fortis, 18.11.2025

-

8. Innovative digital payment wallet Wero arrives in Luxembourg, EPI, 16.06.2025

-

9. iDEAL to phase into Wero starting in 2026

-

10. iDEAL wordt Wero, Wero-wallet.eu

-

11. RBI joins the European Payments Initiative as Acceptor PSP, Raiffeisenbank International 26.11.2026

-

12. PSA prepares issunig support for Wero in Austria and Germany / PSA bereitet Issuing-Support für Wero in Österreich und Deutschland vor, PSA, 23.01.2026

-

13. Bancomat, Bizum, EPI, SIBS and Vipps MobilePay sign MoU to accelerate the rollout of sovereign, pan-european payment solutions, EPI, 02.02.2026

-

14. EuroPA and EPI Confirm Commitment to Expand Sovereign Pan-European Payments with a Hub model, EPI, 02.09.2025

-

15. Europäische Zahlungsdienste beginnen Kooperation, Handelsblatt, 05.02.2026

-

16. Stellungnahme von EPI zum Digitalen Euro“, Deutscher Bundestag

-

17. Das Surcharge-Verbot in Gestalt der PSD3 / PSR, paytechlaw, 04.03.2023