Instant Payments Regulation: Implementing Reporting Requirements Efficiently – Excel Upload or an Integrated Reporting Solution?

The Instant Payments Regulation supplements the existing SEPA Regulation with new, uniform reporting requirements (regulatory reporting). In the future, payment service providers must submit their data in a structured format to the relevant national supervisory authority. What does this mean for banks?

Included in this collection:

Open collection

E-Invoice 2026+: A requirement for businesses – a strategic opportunity for banks and payment service providers

SEK, DKK, NOK: How ISO 20022 connects Nordic payments to your ERP

The Digital Euro versus Consumer Payments – an unnecessary controversy

Beyond Borders – Corporate Survey Results Unpacked

Instant Payments Regulation: Implementing Reporting Requirements Efficiently – Excel Upload or an Integrated Reporting Solution?

Another step toward implementation: The ECB’s digital euro pilot program launches

FiDA and Open Finance: When data becomes a competitive advantage

DTAZV will be phased out in November 2026 – here's what Corporates and SAP Customers need to prepare for now

The digital euro in everyday payments

Wero 2025/2026 – The European payment engine is picking up speed

Spotlight

What is the Instant Payments Regulation?

The Instant Payments Regulation is an EU regulation that requires payment service providers to offer SEPA instant credit transfers as the standard starting in 2025, ensuring that transactions are processed within 10 seconds, 24/7.

What reporting requirements does the Instant Payments Regulation impose on payment service providers?

The Instant Payments Regulation requires payment service providers to submit annual reports to the competent authorities. These include, among other things:

- the number and volume of credit transfers and instant credit transfers,

- the fees for credit transfers and instant credit transfers,

- the fees for payment accounts, and

- the number of rejected payment executions that were denied due to targeted financial restrictive measures.

To whom and in what form must the reports be submitted?

The reports must be submitted to the national supervisory authorities; in Germany, this is BaFin. Acceptable methods include either uploading a completed Excel template via the MVP portal or submitting an automated report via reporting software.

With the Instant Payments Regulation (EU) 2024/886, the European Union has established mandatory rules for the use of instant credit transfers (instant payments) within the SEPA area. While many payment service providers already implemented the operational aspects—such as 24/7 processing, verification of payee, or adjustments to sanctions screening—last year, another aspect has come into the focus of supervision since April 9, 2026: regulatory reporting.

The Instant Payments Regulation supplements the existing SEPA Regulation with new, uniform reporting requirements. Going forward, payment service providers must submit their data in a structured format to the relevant national supervisory authority. In Germany, submissions are made via BaFin and the MVP portal. The first report was due by April 9, 2026 at the latest and covers a retroactive period starting October 26, 20221.

New Reporting Requirements Under the Instant Payments Regulation

The legal basis for the reporting requirement is Article 15(3) of the SEPA Regulation, as amended by Regulation (EU) 2024/886. Accordingly, payment service providers are required to submit annual information on:

- the number and volume of credit transfers and instant credit transfers,

- the fees for credit transfers and instant credit transfers,

- the fees for payment accounts,

- as well as the number of rejected payment executions that were denied due to targeted financial restrictive measures.

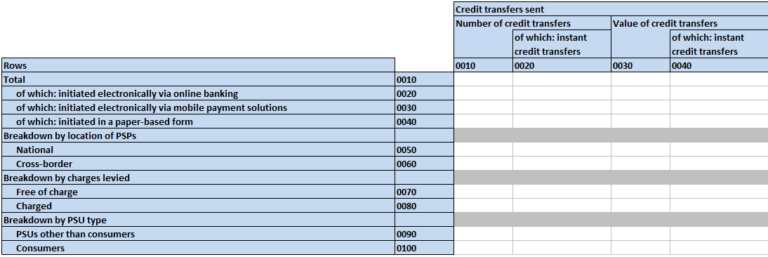

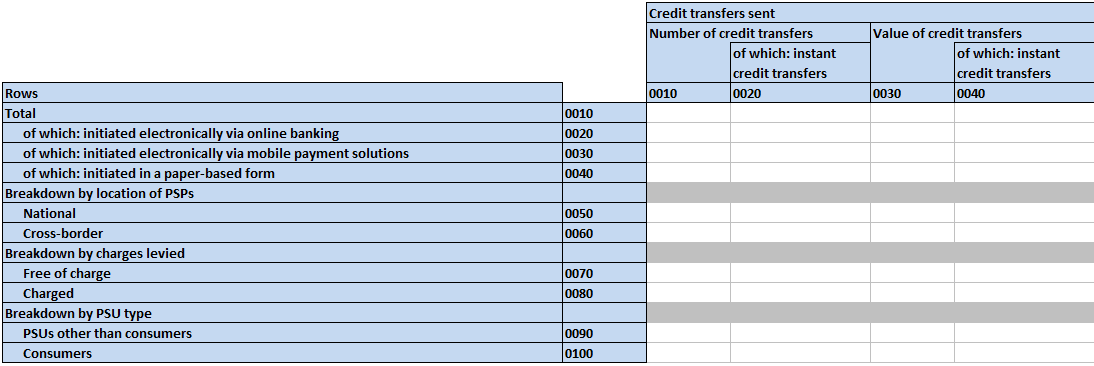

The data on the number and volume of (instant) transfers must be reported separately according to the recipient’s location (domestic, cross-border), the fees charged (free of charge, subject to fees), and the customer type (retail customer, corporate customer).

Figure 1 shows an excerpt from the corresponding BaFin reporting sheet for outgoing transactions. Similar breakdowns must be provided when reporting information on fees, while rejected payment executions are distinguished according to the institution responsible (Payers’ PSP, Payee’ PSP).

Figure 1: Excerpt from the BaFin reporting form “S 01.01 – Number and Value of Credit Transfers and Instant Credit Transfers”

Data is collected on a calendar-year basis; reporting formats are standardized and subject to strict plausibility and validation rules1. The aim of the regulation is to ensure transparency regarding the pricing, usage, and impact of instant payments in the European payments system. National supervisory authorities forward the aggregated information to the European Commission and the European Banking Authority (EBA)2.

Two Ways to Submit a BaFin Report

For the technical implementation of reporting requirements, BaFin provides for two permissible submission methods:

- Uploading a completed Excel template via the MVP portal

- Automated reporting via reporting software, for example within existing reporting systems

According to the Instant Payments Regulation, both methods are equally permitted under regulatory standards—but differ significantly in terms of operational effort, scalability, and integration into existing processes.

Excel upload: Regulatorily permissible, operationally demanding

The Excel-based reporting method uses a template provided by BaFin, which must not be structurally altered and is subject to predefined validation and plausibility checks during upload. The file must be uploaded via the MVP portal and forms the formal basis of the report1.

From a project perspective, it is evident that this approach may be particularly suitable for institutions with low complexity or as a short-term entry-level solution. At the same time, it involves a significant amount of manual effort that should not be underestimated. The required information must be consolidated from various source systems, correctly aggregated, and consistently maintained across multiple reporting years. Changes to fee models, product structures, or sanctioning logic directly impact the reporting logic and increase the need for coordination between business units, IT, and reporting.

In addition, technical inquiries or validation errors often require in-depth regulatory knowledge. While the Excel template provides formal checks, it does not replace subject-matter expertise or audit-proof traceability over extended periods.

BaFin makes the currently valid and up-to-date version of the upload file available on the MVP portal3. This means it must be reviewed annually for potential changes, and the reporting and calculation logic must be adjusted accordingly as needed.

Automated Reporting as Part of the Reporting Architecture

Against this backdrop, many institutions are relying on an integrated solution for regulatory reporting. Reporting software, such as BAIS, enables the requirements of the Instant Payments Regulation to be embedded directly into existing reporting processes4. The calculation of reporting metrics is rule-based and drawn from the central data repository, including validations, historical tracking, and transparency down to the individual transaction level.

The approach presented on Banking.Vision demonstrates how Instant Payment Reporting can be seamlessly integrated into an established reporting environment5. This ensures that reporting is not treated as an isolated obligation, but rather as an integral part of a consistent overall regulatory architecture.

Such an approach becomes particularly important when reporting is designed to be annual, audit-proof, and expandable in the future – for example, with regard to additional EBA standards or future requirements from PSR and PSD3.

Which solution is right for which institution?

In practice, there is no one-size-fits-all recommendation. Rather, the choice of reporting channel depends on several factors:

- The Excel upload can be useful if

- the volume of reports is manageable,

- the immediate priority is to formally comply with the obligation,

- or a central reporting infrastructure does not yet exist.

- An integrated reporting solution is recommended if

- reporting processes are to be designed to be sustainable, repeatable, and audit-proof,

- other regulatory reports are already being generated automatically,

- or further regulatory expansions are expected in the medium term.

Conclusion: Reporting is more than just a formality

With the Instant Payments Regulation, a new phase of regulatory transparency is beginning for many payment service providers. Reporting requirements are not a one-time project, but rather part of an ongoing regulatory dialogue between institutions and regulators.

With experience in both Excel-based reporting procedures and the integration of automated reporting solutions, msg supports institutions as a consulting partner in selecting and implementing a suitable reporting approach. The decisive factor here is not the tool alone, but a clearly defined target vision that harmonizes regulatory requirements, data availability, and operational processes.

Sources

-

1. Reporting Requirements under the Regulation on Real-Time Transfers, BaFin, April 14, 2026

-

2. Regulation (EU) 2024/886 of the European Parliament and of the Council, Official Journal of the European Union, March 19, 2024

-

3. Excel Template: Fees for Credit Transfers, Real-Time Transfers, and Payment Accounts, as well as the Percentage of Declined Payment Transactions (MVP Portal), BaFin, April 14, 2026

-

4. BAIS Reporting software for satisfied customers, msg for banking

-

5. Instant Payments Regulation Reporting – ready for the new EU reporting requirements?, Banking.Vision, 2026-02-26

-

6. PSD3 and PSR on the home stretch: now is the time to prepare, Banking.Vision, 2026-02-09