AI Governance in Banking: Why Control Determines Customer Trust

AI governance in banking determines whether artificial intelligence builds trust or destroys it. Anyone who cedes control here loses far more than just efficiency — they lose customer acceptance. Read on to learn why controllability, accountability, and data sovereignty are now becoming the core of banking.

- AI Acceptance Tracks the Sense of Control, Not Capability

- What Control Actually Means for Customers

- AI Governance in Banking: Regulation and Customer-Centricity Pursue the Same Goal

- AI Is Already Active on Both Sides of the Customer Conversation

- AI Governance Starts Where Data, CRM, and Accountability Converge

- Quellen

AI is changing how decisions get made in banking — but not who is responsible for them. Liability, trust, and accountability remain with the bank. What has shifted is the nature of decision-making itself: prepared, contextualised, and in some cases pre-structured by systems whose internal reasoning is not fully visible.

For customers, what proves decisive is not the systems’ capabilities, but the confidence that control is retained.

The central question of AI governance is therefore not how much automation is technically possible. It is: how much control remains? Banks that introduce AI without answering this question are displacing risk, not reducing it.

Research on the connection between AI and IT governance is consistent: what determines AI success is not system performance, but the quality of its integration into clear decision-making and accountability structures. Where those structures are absent, opacity and loss of control follow as systemic consequences, not isolated incidents. ¹

On the customer side, the question becomes concrete.

AI Acceptance Tracks the Sense of Control, Not Capability

Customers do not approach AI with a fixed stance. Their response is situational. In service processes (account queries, account opening, document handling) AI is experienced as useful friction removal. It saves time and speeds resolution.

When decisions become financially consequential or difficult to reverse, that picture shifts. Hesitation emerges: not primarily because of inaccurate results, but because of the feeling of losing control. Acceptance research confirms this directly — systems are rejected less because of errors than because of the absence of any ability to intervene. ²

Channel preference reflects the same dynamic. Text-based interactions are favoured over voice-based ones, because text can be read, reviewed, and corrected; speech feels transient and harder to govern. ³

Precision alone is not enough. What drives acceptance is the sense that intervention is always possible.

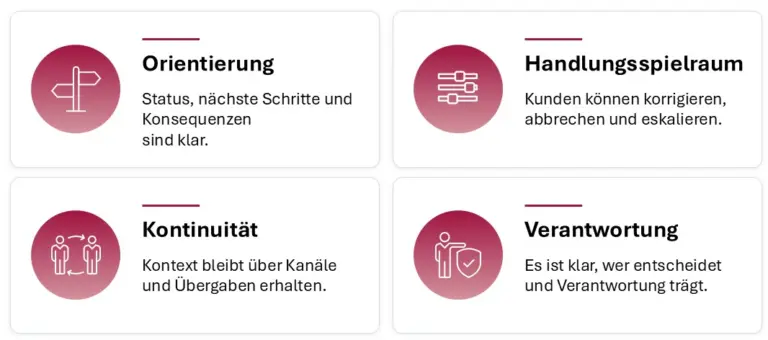

What Control Actually Means for Customers

Transparency and control are not the same thing. Transparency makes a system explainable. Control gives people the ability to act within it. For customers, the latter is what counts.

They do not need to understand how a model works. They need confidence they can intervene, and that a person is accountable when it matters.

Four factors make control tangible in practice:

When any of these is absent, distrust compounds. The technology is rarely the actual problem. The absence of boundaries around its use is. This need for control is not a customer preference in isolation. It aligns directly with regulatory requirements.

AI Governance in Banking: Regulation and Customer-Centricity Pursue the Same Goal

Regulatory requirements such as the EU AI Act demand human oversight, traceability, and clear accountability in AI-supported decisions. ⁴ In the DACH region, BaFin has elaborated these expectations specifically for the financial sector. ⁵ These are not abstract compliance demands. They are the formalised response to exactly what customers already expect.

AI governance does not act as a constraint on innovation, but as the framework that makes sustainable AI adoption possible. Banks that build AI along these guardrails from the outset create more stable and scalable solutions.

Data sovereignty is no longer a secondary concern. Who controls data and how it is used is not a standalone compliance matter — it is part of the AI governance logic itself and a central determinant of trust. Personalisation illustrates the stakes: without clear data ownership, it becomes a black box. With it, personalisation can work the opposite way: relevant, traceable, and acceptable to customers.

Governance structures also carry economic weight, as empirical evidence suggests. Banks with stable frameworks around ethics, accountability, and controllability demonstrably outperform those focused primarily on technical capability. ⁶

AI adoption does not create value on its own. The way it is organised does.

AI Is Already Active on Both Sides of the Customer Conversation

Banking is no longer the only party in a customer interaction deploying AI. Customers now use it independently — to research options, compare offers, and prepare before they speak to an advisor. At the same time, advisors draw on AI-supported tools to structure conversations and derive recommendations.

A concrete example: a customer arrives at a mortgage advisory meeting with an AI-generated assessment from a comparison platform. The advisor is working with a system that produces recommendations from product parameters and risk profiles. Both are starting from AI-mediated positions, from different data sources, with different underlying logic.

For the customer, this is not an abstract system design question. It is uncertainty in one of the most significant financial decisions of their life.

When these perspectives meet without coordination, contradictory expectations arise. The conversation loses credibility, not through error, but through misalignment.

Banks that do not actively govern this dynamic lose more than operational efficiency. They lose the coherence of the customer dialogue and with it their standing as a trusted partner in the moments that matter most to customers.

AI Governance Starts Where Data, CRM, and Accountability Converge

The implication is direct: AI must be orchestrated. That means a continuous control logic defining how data is used, how decisions are formed, and who can intervene at which point. Data sovereignty is not a separate step in this process, but part of that logic itself.

In banking, this control logic becomes concrete where customer data, consents, interaction history, and advisory responsibility converge: in the CRM as the operational core of governance. Isolated AI deployments do not resolve this. They shift the problem elsewhere.

Without an overarching governing principle, inconsistencies compound. Statements contradict, context disappears, accountability grows diffuse.

This governance logic requires an organizational anchor point. A system that not only stores customer data, consent records, interaction history, and responsibility for consultations, but also consolidates them and makes them manageable. Platform solutions such as the BSI Customer Suite address this need precisely.

The success of AI in banking will not be determined by how autonomous systems can become. What matters is how clearly responsibility remains organised.

Progress comes from precisely defined control — not maximum automation.

Responsibility cannot be automated.

Sources

-

1. Merve Kacar, Application of AI in Customer Experience Management. In: Hannig, U., Seebacher, U. (eds) Marketing and Sales Automation, 2023.

-

2. Gabi Schaap, Tibor Bosse & Paul Hendriks Vettehen, The ABC of algorithmic aversion: not agent, but benefits and control determine the acceptance of automated decision-making, 2023.

-

3. Acxiom, AI-curated experience in banking, 2026.

-

4. EBA, AI Act: implications for the EU banking and payments sector, 2025.

-

5. BaFin, KI bei Banken und Versicherern: Automatisch fair?, 2024.

-

6. Pedro Machado, Technology is neutral, governance is not: AI adoption in the banking sector, 2026.

-

7. Svetlana Sitnicka, Muslum Mursalov, Hamdulla Mammadov, Denys Babaiev, Yong Zhou, Ethics, Institutions, Infrastructure, and Governance in AI National-Level Readiness: A Hidden Driver of Banking Transformation, 2025.

-

8. Anjum Razzaque, Artificial Intelligence and IT Governance: A Literature Review. In: Musleh Al-Sartawi, A.M.A. (eds) The Big Data-Driven Digital Economy: Artificial and Computational Intelligence, 2021.