SEK, DKK, NOK: How ISO 20022 connects Nordic payments to your ERP

Connecting Scandinavia in your ERP – with ISO 20022 and structured payment references. How Nordic payment systems work in practice.

Included in this collection:

Open collection

Quantum Key Distribution in Banking – New Security Standard or Niche Solution?

E-Invoice 2026+: A requirement for businesses – a strategic opportunity for banks and payment service providers

SEK, DKK, NOK: How ISO 20022 connects Nordic payments to your ERP

The Digital Euro versus Consumer Payments – an unnecessary controversy

Beyond Borders – Corporate Survey Results Unpacked

Instant Payments Regulation: Implementing Reporting Requirements Efficiently – Excel Upload or an Integrated Reporting Solution?

Another step toward implementation: The ECB’s digital euro pilot program launches

FiDA and Open Finance: When data becomes a competitive advantage

DTAZV will be phased out in November 2026 – here's what Corporates and SAP Customers need to prepare for now

The digital euro in everyday payments

From 15 November 2026, only structured or hybrid address formats may be transmitted in SEK and SEPA payments. For companies with subsidiaries or business relationships in Sweden, Denmark or Norway, this is a hard deadline – and at the same time a compelling reason to fundamentally reassess their payment infrastructure. The “Nordic bloc” – Sweden, Denmark, Norway and Finland – remains strongly shaped by country-specific practices despite its highly modern banking landscape: the systems differ considerably in structure, clearing mechanisms and messaging logic. The Nordic Payments Council (NPC) develops and harmonises payment standards and initiatives specifically for the Nordic countries. 2026 marks a turning point: Swedish banks are currently migrating to a new payment infrastructure based on ISO 20022 and the NPC Nordic Rulebook scheme.

This article examines the specifics of Nordic payment systems – and the new opportunities the ISO 20022 migration brings with it. Corporate clients already processing SEPA payments via their ERP system can connect Sweden, Norway and Denmark with manageable effort.

ISO 20022: The key changes at a glance

- The Bankgiro system – the most important clearing house for Swedish retail payments – is currently undergoing extensive modernisation. Several legacy formats will be by end of 2026 discontinued and replaced with ISO 20022.

- From November 2026, only structured or hybrid address formats may be transmitted in SEPA and SEK payments.

- For payments to Denmark, these address requirements take effect in the first half of 2027.

What does this mean for companies expanding into Scandinavia?

Many German companies operate subsidiaries, production sites or sales offices in Scandinavia. With the exception of Finland, Sweden, Denmark and Norway all have their own currencies. Since Finland uses the euro, payments there can be processed through SEPA in the usual way. For the other Nordic countries, the situation is different.

Anyone making payments from Germany in SEK, DKK or NOK must rely on cross-border payments. At high payment volumes over the long term, this can become costly. SEPA benefits such as instant payments and Verification of Payee are also unavailable for these three countries.

Direct connectivity to local payment infrastructures would enable payments in Nordic countries without routing via SEPA or correspondent banks. Companies benefit not only from lower bank fees and faster processing, but also from the ability to harmonise payments via a unified XML format.

Nordic Payment Systems at a glance

Finland

- Domestic payments in Finland are executed as SEPA–credit transfers.

- In addition to SEPA requirements, Finnish banks may agree on so-called Additional Optional Services (AOS) to enable the exchange of additional information – such as Extended Remittance Information (ERI) – allowing originators to include multiple invoices or credit notes in a single transfer, with detailed information on each invoice.

- The use of SEPA-Lastschriften is less widespread in Finland than e-invoicing (E-Invoice). Invoices are sent digitally and can be imported directly into recipients’ accounting systems. Finvoice, developed by Finnish banks, is a leading e-invoicing standard in Finland.

Sweden

- All payments in Swedish kronor (SEK) are settled via RIX – the settlement system of the Swedish central bank Sveriges Riksbank.

- Companies wishing to use Swedish payment systems require a SEK-Konto bei einer Bank mit Niederlassung in Schweden.

- Bankgiro is the most widely used credit transfer scheme in Sweden, processed via the Bankgirot Clearing-System. As part of the payment infrastructure modernisation, many existing Bankgiro products and formats will be discontinued by end of 2026.

- Additionally, the PlusGiro-System, owned by Nordea, exists alongside Autogiro, the Swedish direct debit scheme.

- Sweden is systematically modernising its payment infrastructure towards Instant Payments. RIX-INST basiert auf der europäischen TIPS-Plattform des Eurosystems und war der erste Nicht-Euro-Markt, der in TIPS integriert wurde. Der Nordic Payments Council (NPC) is also actively developing an NPC Verification of Payee (NVOP) Scheme for local payments in Nordic countries.

Denmark

- All domestic payments in Danish krone (DKK) must be processed between bank accounts held in Denmark.

- The FIK-method – operated by Mastercard Payment Services – is the central OCR-reference-based payment system for business invoice payments and enables fully automated payment reconciliation.

- Betalingsservice is the Danish direct debit scheme, used by over 90 % of all Danes for recurring payments such as insurance, subscriptions and instalments.

- With the introduction of Express Clearing (Straksclearing) in 2014, Denmark was a European pioneer in instant payments. Straksclearing allows instant transfers up to a maximum of DKK 500,000.

- Straksclearing was replaced in 2025 by the European TIPS-Plattform (TARGET Instant Payment Settlement) abgelöst, which also processes instant payments in DKK. This marks a significant step towards a unified European payment infrastructure.

Norway

- All domestic payments must be made in Norwegian krone (NOK) between accounts held in Norway. Companies therefore require a NOK account at a bank with a Norwegian presence.

- KID-Payments are a form of giro payment based on OCR technology that use a KID-Number (Client ID) as a reference. This unique number identifies the payer and transmits payment information such as the invoice number. Like the FIK scheme in Denmark, KID payments are operated by Mastercard Payment Services.

- Norway is among the European Vorreitern bei Echtzeitzahlungen: since 2013, Norwegian individuals and companies have been able to make instant transfers via the clearing system „Straks”, which was updated to Straks 2.0 in 2020. The inclusion of NOK in the TIPS platform is planned for the first half of 2028.

- In Norway, the direct debit scheme AvtaleGiro is used for recurring payments (e.g. rent, subscriptions). There is also Autogiro, a direct debit scheme used exclusively in the B2B sector.

The key difference from SEPA: Structured payment references

Each Nordic country has developed its own B2B payment schemes. What they share is the use of an OCR reference number in invoice data to enable automatic payment identification. This system was introduced in Finland in the 1960s and forms the foundation on which all other Scandinavian schemes are built. Whether in account transfers, payment slips or local direct debits, the payment reference is an established market standard and the central element of automated payment reconciliation in accounts receivable management.

The most widely used payment scheme in Schweden is Bankgiro, through which virtually all SEK transfers between companies and their customers in Sweden are processed. It allows companies to settle invoices via a Bankgiro-Nummer.

In Sweden, the Bankgiro number acts as an alias for the bank account number – a company can have a single Bankgiro number. This enables a company to change banks without changing its payment address.

The invoice states an OCR-Number , which serves as a unique payment reference. This reference enables automatic matching of payments to open invoices. Norway uses a similar model with the KID-Number (“Kundeidentifikasjon”).

In Denmark the FIK-System is used, available in three variants (payment form type 71, 73 and 75) depending on whether a free-text message alongside the OCR reference is supported. In FIK, a vendor ID (similar to the Bankgiro number) identifies the payee.

FIK 71

→ OCR-based payment

→ Focus on automated posting (e.g. invoice payments)

FIK 73

→ Freitext- Zahlung

→ Used when the payee is unknown or additional information is required.

FIK 75

→ Hybrid solution

→ Combines OCR payment reference + optional message (typical in B2B)

Finland offers, as a supplement to SEPA, the AOS service Extended Remittance Information (ERI, which allows originators to use a reference number (Referenznummer (viitenumero) to transmit invoice information.

Looking at Germany,, invoice numbers can be included unstructured in the SEPA reason for payment. The remittance field is limited to 140 characters, so with batch payments not all invoice references can always be transmitted. In such cases, a “Zahlungsavis” (Remittance Advice) is used, containing a detailed breakdown of settled invoices.

Remittance advices are generated automatically in ERP systems such as SAP during the payment run and sent to the payee, typically by email or in a structured format (e.g. EDI). Bank statements for batch payments generally show only a total amount. The remittance advice enables the associated open items to be identified and matched accordingly.

Comparison of Nordic payment reference systems

| Dänemark | Schweden | Norwegen | Finnland | |

| FIK | OCR-nummer | KID | Viitenumero | |

| Recipient bank details | Creditor number / account number | Bankgiro-Nummer | Kontonummer | IBAN |

| Reference types | 3 types (71, 73, 75) | Uniform | Einheitlich | Einheitlich |

| Reference length | 15 digits + 1 check digit | 2–25 digits | 2–25 Stellen | 3–20 digits |

| Algorithm | Modulus-10 | Modulus-10 | Mod-10 / Mod-11 | Modulus-10 |

| Alias layer | Kreditornummer | Bankgiro-Nummer | Direct account number | Direct IBAN |

How Automated Payment Reconciliation with Payment References Works

- The creditor first creates an invoice, generating a payment reference that is printed on the invoice.

- The debtor then transfers the amount due, including the payment reference.

- The bank automatically forwards this reference together with the payment.

- The creditor then receives a bank statement (CAMT.053 Datei) in which payment references are matched to the corresponding transactions.

- The ERP system identifies the OCR number and automatically matches the payment to the corresponding open invoice.

- For batch postings, individual transactions are itemised using the OCR-Datei, die von der Bank zur Verfügung gestellt wird.

- This enables posting and account clearing to be fully automated.

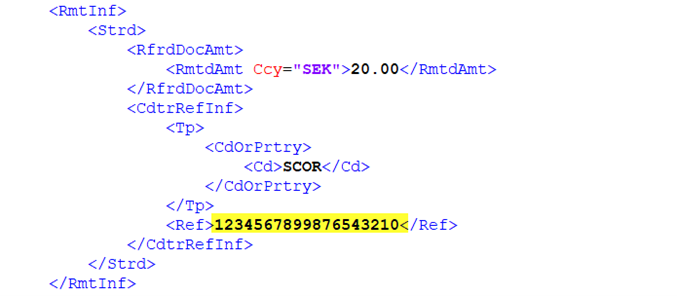

ISO 20022 – Payment reference in the structured remittance field

In the pain.001 message, payment references must be stated in the structured remittance field. A single payment line item can contain multiple invoices and payment references. A single XML payment entry can hold up to 999 invoices.

Abbildung 1: Beispiel Strukturierte Verwendungszweck mit Zahlungsreferenz

ISO 20022 – Payment reference in the structured remittance field

Each structured remittance entry corresponds to one invoice and contains the following elements:

- Amount: depending on the XML field, the bank interprets the amount as negative or positive:

- <RmtdAmt> – invoice amount

- <DuePyblAmt> – amount due

- <CdtNoteAmt> – Gutschrift

- Reference number: <CdtrRefInf><Ref> – Norwegian KID number, Swedish OCR number, Finnish viitenumero and Danish FIK number

- Document indicator: the value “SCOR” must be set when using the payment reference

The Nordic banking system validates on every payment whether the sum of <RmtdAmt>, <DuePyblAmt> and <CdtNoteAmt> matches the transfer amount <InstructedAmount>. If the amounts do not match, the payment is rejected.

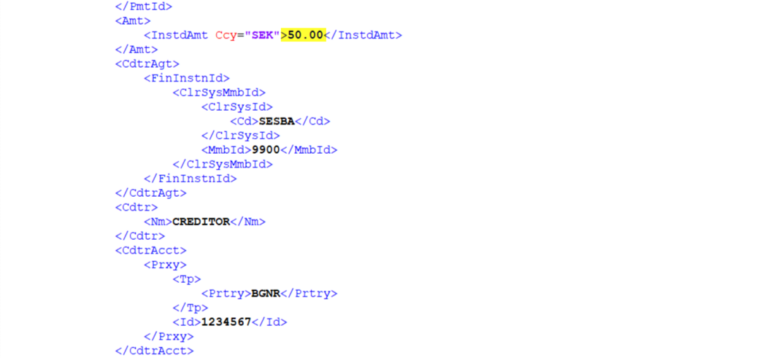

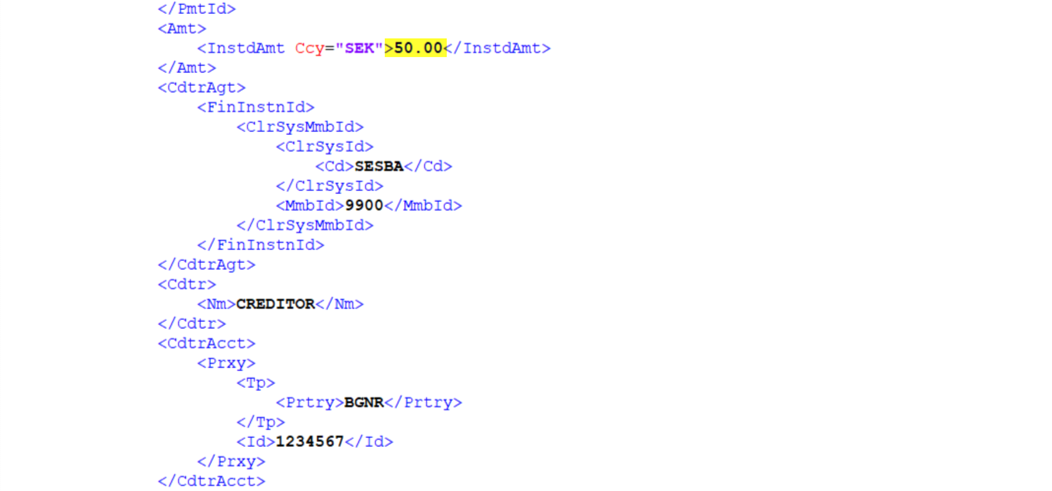

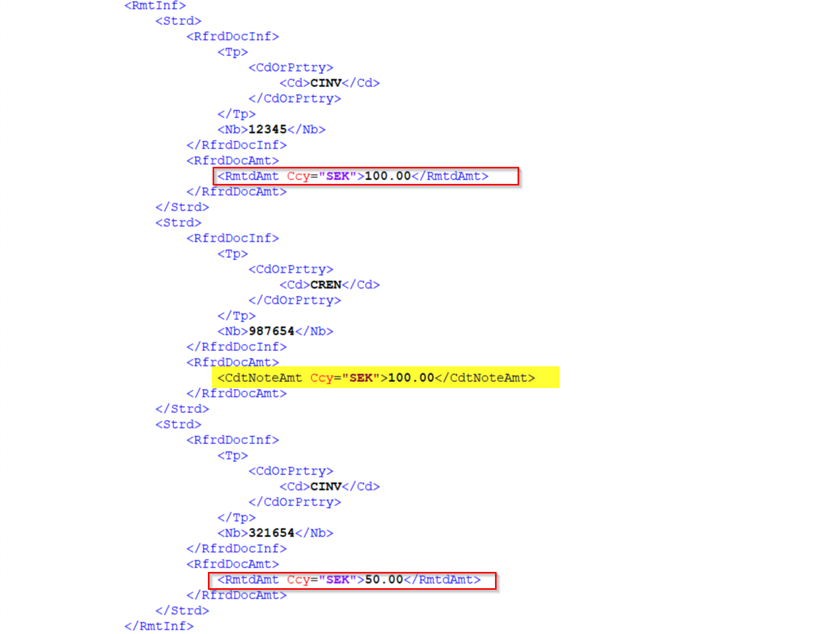

Example: We have a transfer with an amount of SEK 50.00.

Abbildung 2: Ausschnitt aus einer Bankgiro-Überweisung in pain.001 Format

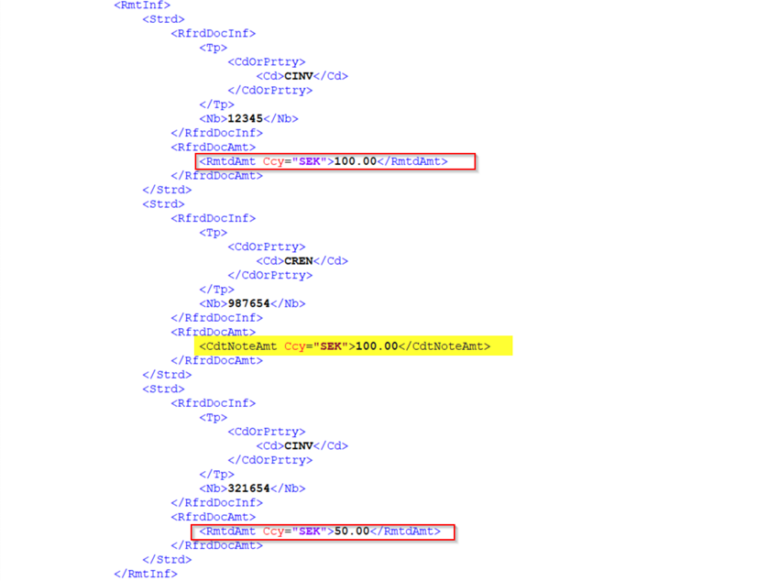

The amount of SEK 50.00 is made up of the following items: two invoices totalling SEK 150.00 and a credit note over 100,00 SEK. After subtracting the credit, the total comes to 50.00 SEK. Credit notes are referenced with the code CREN and receivables with CINV (Invoice).

| POSITION | TYP | <RefDocInf> | BETRAG |

| Rechnung 1 | Receivable (Invoice) | CINV | +100,00 SEK |

| Credit Note | Credit (Credit Note) | CREN | -100,00 SEK |

| Invoice 2 | Receivable (Invoice) | CINV | +50,00 SEK |

| SUMME | +50,00 SEK |

Abbildung 3: Beispiel Strukturierte Verwendungszweck mit Invoice und Credit Note

Technical implementation in SAP

Integrating Nordic payment references into the SAP payment module (SAP S/4HANA or ECC) requires targeted configuration steps. The following guidance is aimed at SAP-responsible teams – treasurers, project managers and consultants with SAP payment module expertise. Country-specific OSS-Hinweise should be implemented. Supporting functions – such as payment reference validation (e.g. modulo-10/modulo-11 checks) – are partially available via OSS notes or via standard functions and customer-specific enhancements (BAdIs/User-Exits).

In addition, the Payment Medium Workbench (PMW) and corresponding DMEE-Format-Trees must be configured so that payment references are correctly mapped to the designated XML fields.

Key steps in electronic bank statement processing (EBS) include mapping references to SAP fields and configuring interpretation algorithms (e.g. in OT83). The objective is to automatically match payments to open items using reference numbers.

As the source of the payment reference, SAP typically uses document or master data fields (e.g. XBLNR or ZUONR). For Denmark and Norway, the field FEBEP-KIDNO is commonly used, as it is specifically designed for structured references (KID/FIK). vorgesehen ist. In Sweden werden hingegen häufig die Felder XBLNR und ZUONR are used instead, as no dedicated KID field is strictly required.

Conclusion

ISO 20022 brings payments in Sweden, Denmark, Norway and Finland to the same technological level as SEPA – but with greater granularity, more structure and significantly higher automation potential.

Integrating Nordic countries into SAP requires targeted extensions to existing payment processes. The greatest value lies in using structured payment references, which enable near-complete automation of incoming payment processing.

For companies, this means: those who prepare their ERP system methodically can implement the transition efficiently and with minimal risk – while gaining access to one of the most efficient payment infrastructures in Europe.

Want to learn more?

We support both banks and corporate clients on topics including EBICS, Verification of Payee and payment format migrations in SAP.r Zahlungsformat-Umstellungen in SAP.