Digital Customer Loyalty: Focusing on Young Customers

Customer loyalty starts early. Young customers expect simple digital experiences rather than immediate advisory appointments. Regional banks can build trust through digital customer experiences and stay relevant during their customers’ most financially important life stages.

- Why early digital support determines customer loyalty in banking

- Expectations of young customers

- Long term value of retaining young customersLong term value of retaining young customers

- Building trust through digital support

- Use cases for digital engagement

- How banking.X.hub supports these requirements

- Key implications for regional banks

Why early digital support determines customer loyalty in banking – Young customers and changing banking behavior as a strategic challenge

Regional banks have traditionally maintained strong relationships with younger customers. Many people come into contact with a local bank early in life through their family, school, clubs, or other local activities.

However, this early connection is not enough to ensure long-term loyalty. Young customers are willing to switch banks if the digital experience does not meet their expectations. This is usually not driven by dissatisfaction with regional banks themselves, but by a preference for convenience. At this stage of life, digital services are far more important than physical branches. Customers expect easy to use applications, affordable account models, and clear structures that help them manage their finances without effort.

The key objective for regional banks is therefore not primarily to acquire new customers, but to maintain the trust established early on and develop it into long term, profitable relationships. A strong digital experience at an early stage creates the foundation for trust and ensures continued relevance throughout important life phases.

Expectations of young customers

Young adults expect banking to fit naturally into their everyday digital life. They are used to intuitive and seamless experiences from other digital services such as streaming, online shopping, and social media.

Interest in financial topics exists, but it is often still at an introductory level. For everyday banking, the following aspects are particularly important:

- intuitive usability

- clear and understandable information

- transparency

- step by step digital guidance

- support through digital tools instead of immediate personal consultation

For more complex topics such as retirement planning, insurance, or property financing, personal advice remains relevant. However, it is usually expected only after the basic knowledge has already been built digitally.

As customers move into later stages of life, personal interaction becomes more important. The initial engagement, however, almost always takes place digitally.

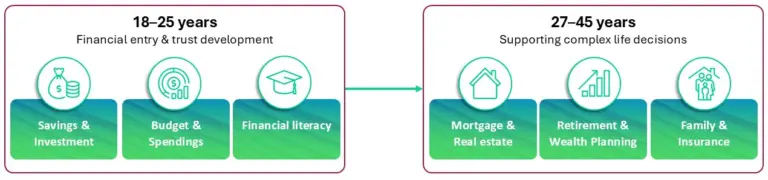

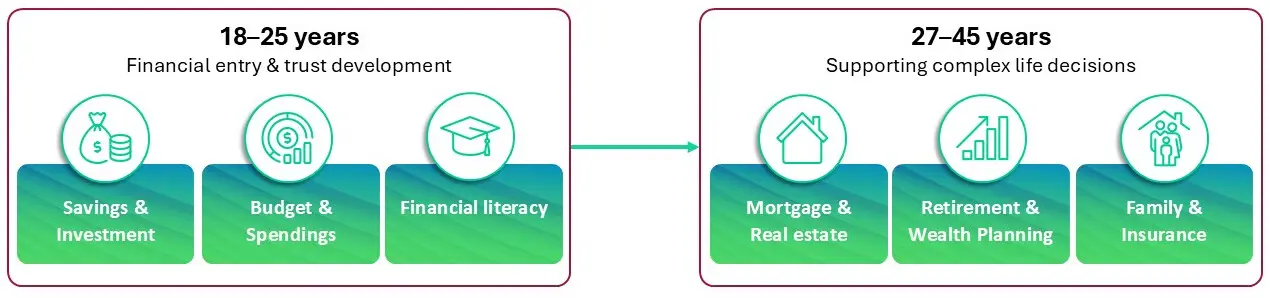

Figure 1: Needs of young customers

Long term value of retaining young customers

The way banks engage with young adults has a direct impact on their long-term success. Financial capacity is often limited between the ages of 18 and 25. Between 27 and 45, however, customers enter a phase in which major financial decisions are made. These include starting a family, financing property, building wealth, and planning for retirement.

Banks that fail to establish strong relationships early on are unlikely to benefit from these later opportunities. Switching to another provider is easy if the onboarding and digital experience are simpler elsewhere. Once customers leave, they rarely return, even if they later require financial advice.

Regional banks benefit from building trust early and demonstrating reliability and clarity. What matters is a simple entry point that allows customers to grow into more complex services over time.

Building trust through digital support

Young customers are open to financial topics when they are presented in a practical and accessible way. Digital services can provide real value by offering a clear overview of finances, helping with budgeting, supporting savings goals, and introducing basic investment options. They can also address financing needs for first larger purchases such as furniture or a car.

Clear interfaces, understandable explanations, and relevant suggestions help create trust. When banks focus on supporting customers rather than promoting products, a continuous relationship develops. Personal advice then becomes a natural next step rather than a separate interaction.

Use cases for digital engagement

Use Case: Dynamic segmentation and context-based communication

Segmenting customers according to their current life situation, for example studying, apprenticeship, time abroad, or starting a career, allows banks to offer relevant support. This can be combined with data such as spending behavior, saving patterns, or regular payments.

Based on this, banks can provide:

- automated savings suggestions,

- suitable insurance and investment options,

- budgeting support,

- projections for future expenses,

- reminders related to tax returns.

The goal is to help customers better understand and manage their financial situation, rather than just selling them products.

Use Case: Digital support for saving and investing

Digital tools can identify saving potential and guide customers step by step towards building assets. For example, insights into monthly financial surpluses or spending patterns can help customers recognize opportunities to save.

At the same time, digital support can introduce investment topics in a structured and understandable way. This includes explaining possible investment options, showing realistic development scenarios, and illustrating the impact of small regular contributions. Information about government support schemes can also be included.

Additional formats such as guided questionnaires or digital chat support can help explain basic concepts and reduce uncertainty around financial decisions.

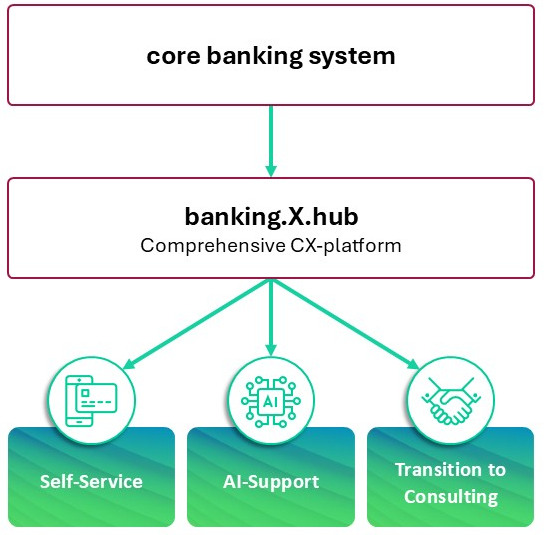

How banking.X.hub supports these requirements

banking.X.hub connects customer and bank data and uses this information to guarantee relevant and timely interactions. It allows regional banks to address customers with content and services that match their current situation.

A native API connection to the core banking system enables seamless data transfer, which makes it possible to use existing systems without major adjustments.

The platform supports:

Figure 2: banking.X.hub helps build customer loyalty

- personalized customer journeys based on life situations

- consistent digital interaction without disruptions

- context related explanations and content

- self-service functionalities

- digital support for financial questions

- selection of the appropriate communication channel

- integration of additional tools

- a smooth transition to personal advice when needed

This leads to higher customer satisfaction and more efficient processes. Retaining existing customers is more cost effective than acquiring new ones, and young customers can already contribute value if services are aligned with their needs.

Key implications for regional banks

Regional banks have an advantage through their local presence and early customer relationships. However, this advantage only translates into long-term success when it is supported by a strong digital experience.

For young customers, digital quality is a basic requirement. It strongly influences whether they remain with their bank or choose a different provider. Personal advice continues to play an important role, but mainly at later stages in life. Banks that lose customers early will find it difficult to win them back.

banking.X.hub offers a practical and scalable way to meet these expectations and support customers with their financial journey.

Get in touch

Customer trust and long-term relationships, including for younger customers, are a priority for your bank? You want to take a closer look at how data can be used more effectively. If you are interested in practical approaches or would like to exchange ideas on current challenges in banking, we are happy to start a conversation and explore suitable solutions together.