Digital euro: Five key decisions for Europe’s financial institutions

As Europe's digital central bank currency, the digital euro is intended to complement cash and offer advantages in terms of resilience, costs and data protection, among other things. With the adoption of the relevant regulation becoming increasingly likely, the pressure on banks to act is mounting. Five key decisions are on the agenda for Europe's financial institutions.

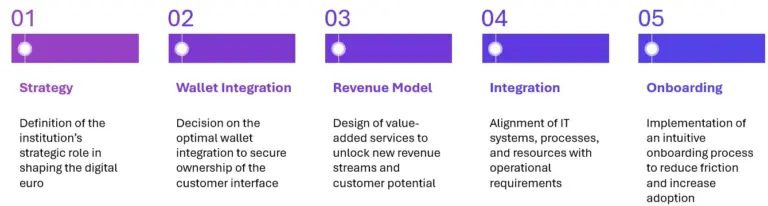

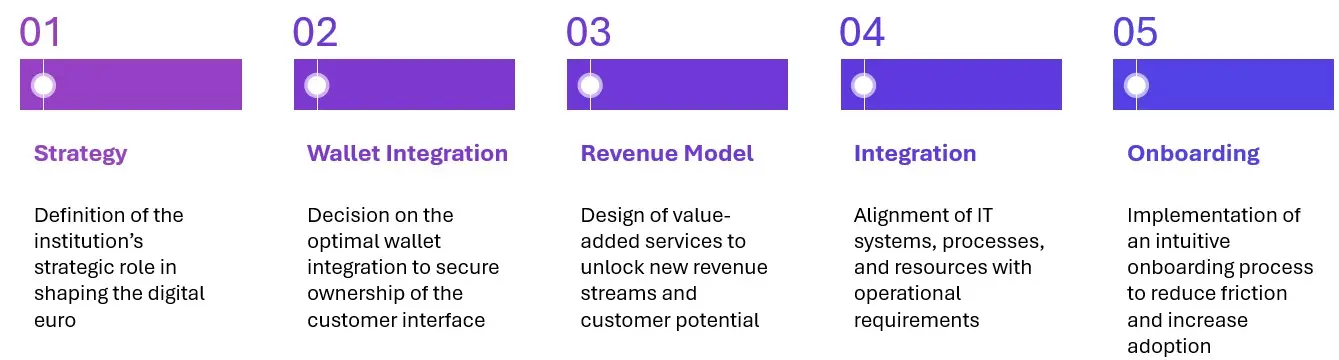

- 1. Banks as Drivers of Innovation or Obligated Implementers

- 2. The Customer Interface as a Competitive Advantage

- 3. Changing Revenue Models in the Digital Euro Ecosystem

- 4. The Challenge of Technical Integration

- 5. Onboarding as the Key to Customer Adoption

- The Digital Euro as a Catalyst for Transformation in Payments

Included in this collection:

Open collection

The digital euro in everyday payments

Wero 2025/2026 – The European payment engine is picking up speed

Digital euro: Five key decisions for Europe's financial institutions

Instant Payments Regulation Reporting – ready for the new EU reporting requirements?

Verification of Payee – a field report

PSD3 and PSR on the home stretch: now is the time to prepare

Digital Euro Unlocked - Report 2026

Payments Radar 2026

Study 2025 on Cross-border Payments from a Business Perspective

FIDA data as the key: How innovative use cases open up new perspectives

For years, the European Central Bank and numerous market participants have been preparing for the potential introduction of the digital euro.

With adoption of the corresponding regulation becoming increasingly likely, the pressure on banks to strategically address the new means of payment is rising. Depending on its specific design, a European central bank digital currency could disrupt the European payments infrastructure and require banks to make fundamental strategic decisions.

What matters for implementation is not only the regulatory dimension but, above all, how citizens will experience and use the digital euro in everyday life.

1. Banks as Drivers of Innovation or Obligated Implementers

One of the most important implications of introducing the digital euro is that banks must clarify their strategic role in the new ecosystem at an early stage.

In the future, the digital euro will coexist with cash and all current forms of digital money transfers such as card payments and bank transfers. It will thus become a new foundational technology that banks with retail customers will likely have to implement. An institution can either become an innovation driver – actively developing new offerings such as value-added services around the digital euro to retain customers – or follow a minimalist implementation strategy. This choice determines how the bank will be perceived in the market. Seamlessly functioning digital euro services will strengthen customer loyalty across a bank’s broader service portfolio.

Ultimately, the wallet, which is the access point to the digital euro, becomes the central hub of the customer relationship. For banks, this is where it is decided whether they remain the primary gatekeeper or are relegated to an interchangeable backend infrastructure provider.

2. The Customer Interface as a Competitive Advantage

Whoever controls the wallet also controls the customer interface, which is decisive for long‑term user retention. Many consumers turn to their house bank to understand, test, and eventually use the digital euro regularly. But if they are disappointed by their bank’s offering while still wishing to use the digital euro, they will inevitably turn to other payment service providers.

Trust is created primarily through simplicity and seamless integration of the digital euro into familiar online‑banking environments. Every additional hurdle increases the risk of a customer giving up. For more analog customer groups, additional support services such as in‑branch consultation or assistance via phone remain essential. Lack of explanations and excessive complexity can reinforce pre‑existing reservations, causing people to stick with familiar payment methods.

A digital euro solution that fails to convince customers could therefore quickly lead them to switch to other providers and thus result in the loss of the customer interface. Switching to a payment service provider outside Europe could even mean that, although the current account remains connected, the customer interface shifts entirely to that provider which is an outcome banks will want to avoid.

Digital Euro Unlocked - Report 2026

Our report offers banks, PSPs and market participants

a clearer understanding of the implications,

responsibilities and strategic decisions they may face

as Europe moves toward a potential retail CBDC – all

grounded in a customer-centric view of the digital euro.

3. Changing Revenue Models in the Digital Euro Ecosystem

The digital euro will transform banks’ revenue models. Although basic functions will remain free of charge for end users, new opportunities may arise through value‑added services. Scenarios such as automatic payment only upon delivery, smart refunds, subscription services, or splitting a bill among a group have already been tested as part of the ECB’s Pioneer Partnership.

msg for banking participated in this innovation platform and developed use cases for conditional payments. Such value‑added services can help banks differentiate themselves from competitors while building new modular revenue models. In addition, digital euro transactions may be processed more efficiently, which could positively affect long‑term cost structures for banks and merchants.

Conversely, revenues from paid SEPA payment receipts for corporate customers may diminish, and – depending on holding limits – some bank deposits may shift into digital euro holdings. Ultimately, the compensation model, especially regarding caps on merchant fees, will determine how the digital euro impacts banks’ income structures.

4. The Challenge of Technical Integration

Beyond strategic and commercial considerations, it becomes clear that integrating the digital euro into existing IT landscapes is a demanding task. The digital euro is not merely an add‑on but a completely new payment infrastructure with its own settlement processes, new wallet functions, real‑time processing, and likely complex offline‑capable mechanisms.

Banks must develop, test, and deploy new systems for wallet management, limit monitoring, and waterfall mechanisms. The waterfall mechanism, in particular, could pose a major challenge because no comparable instrument currently exists. It ensures that digital euro payments can still be executed even when the wallet limit is exceeded, by seamlessly drawing the missing amount from the linked bank account.

The challenges are considerable but manageable. Shared services, white‑label solutions, and partnerships will play a key role in reducing costs and controlling integration efforts.

5. Onboarding as the Key to Customer Adoption

As the fifth key insight, the enormous importance of smooth onboarding must be emphasized. For many customers, onboarding represents their first real interaction with the digital euro, that is the moment where trust is either gained or lost. The process must be as intuitive and frictionless as possible, ideally directly embedded within the familiar banking app, without redundant identification steps, and with clear explanations of core functions such as aliases, holding limits, and automatic top‑ups.

It is useful for essential settings such as linking a current account to be mandatory during first‑time registration. However, more advanced configurations, such as specifying the waterfall mechanism for automatic wallet top‑ups, should not be forced upon users. Default settings can help reduce cognitive load at the beginning. Only when onboarding feels positive customers will continue using the digital euro in their daily lives.

The Digital Euro as a Catalyst for Transformation in Payments

The digital euro is therefore not just a technical infrastructure project but a comprehensive transformation impulse for European payments. It affects strategic positioning, customer experience, revenue models, IT architecture, and how banks define their role within an increasingly digital ecosystem.

Many questions remain open, but the direction is clear: the digital euro is very likely coming, and banks that prepare early can turn it into a competitive advantage.

Comments

Very insightful piece – it finally shifts the discussion from purely technical considerations to practical questions for banks: who do they want to be in the digital euro story – true innovation drivers or merely “obliged backend providers”? The focus on the real battlefield being the wallet and customer interface, rather than the rail itself, is especially valuable: whoever controls the user entry point controls the relationship, not just the transaction flow.

At the same time, in my view the article only touches on, but does not really unpack, two painful topics for banks. First, the risk of losing parts of existing revenue streams (SEPA fees, interchange, etc.) feels much more material than described – particularly for smaller institutions where payments underpin a large share of the operating model. Second, the waterfall mechanism and technical integration with existing cores are not just a “manageable challenge”, but a multi‑year shift in core‑banking, risk and treasury architecture that should be analysed together with tokenised deposits and instant payments.

I fully agree with the closing message: the digital euro is not “just another payment method”, but a trigger to rethink banks’ role in retail payments, trust models and customer experience design. Yet that message will not be enough without an honest scenario analysis for each individual bank: what happens to its balance sheet, revenues and customer interface under an active, minimalist or “late mover” approach to the digital euro ecosystem.