IReF – Pioneer of an Integrated Reporting System (IRS)

The Integrated Reporting System (IRS) is the target vision of a long-term transformation process in regulatory reporting. This article traces the long road to reform since the financial crisis, via IReF to a future IRS.

Included in this collection:

Open collection

The Schufa shadow database: a data protection scandal or a necessity for the credit industry?

High-NPL institution: Requirements for NPL strategy, governance and operational organisation

EBA Supervisory Reporting Simplification or Complication

9th MaRisk Amendment 2026 – Supervisory Briefing: Focus following the consolidation phase

End of support for SAP Bank Analyzer – msg.ORRP as an alternative

Why Europe’s banks need to reassess geopolitical risks

Bundesbank’s Targeted Review of the design of lending guidelines in the LSI environment

AMLR Redefines Risk Analysis: Moving Beyond a Checkbox Exercise – Why Regulators Are Rethinking Their Approach

9th Amendment to the MaRisk 2026: What reliefs does the consultation offer to small and very small institutions (SNCIs)?

Instant Payments Regulation: Implementing Reporting Requirements Efficiently – Excel Upload or an Integrated Reporting Solution?

The ECB’s Integrated Reporting Framework (IReF) marks a profound shift in European regulatory reporting. At the same time, IReF should not be seen as an end point, but rather as a milestone on the path to a significantly more comprehensive Integrated Reporting System (IRS). For banks, this means that regulatory developments must be viewed not in isolation, but as part of a long-term vision.

What exactly do supervisory authorities mean by an Integrated Reporting System (IRS)?

Although it is still too early for a final definition, the current debate is already revealing the key characteristics of such a system:

1. Scope: An IRS must cover at least all traditional reporting domains (i.e., statistical, prudential and resolution reporting).

2. Definitions: A common data dictionary containing uniform and redundancy-free definitions across all reporting domains (define once).

3. Data exchange: Aside from banks’ reporting requirements an IRS also harmonizes the exchange of data between the competent authorities. Ideally, institutions would only need to submit their data to one central data collection point (report once).

4. Granularity: There is broad consensus that future regulatory reporting will be substantially more granular. However, opinions differ on the concrete extent. Certain balance sheet items—such as deposits—may continue to be reported in aggregated form. Moreover, despite increasing granularity, the EBA does not necessarily expect all reporting templates to be abolished.

5. Regulatory changes: In the future, supervisory authorities and legislators are expected to coordinate regulatory changes more closely and rely on the definitions established in the common data dictionary (regulate once). For banks, this means fewer data silos, higher consistency across requirements, and more efficient implementation of regulatory updates.

From today’s perspective, an Integrated Reporting System remains far from current practice. Nevertheless, it is crucial for banks to keep this long-term goal in mind. On the one hand, current regulatory initiatives are already clearly geared towards it (e.g., JBRC), and on the other hand, the IRS provides clear guidance on how institutions can strategically position themselves today.

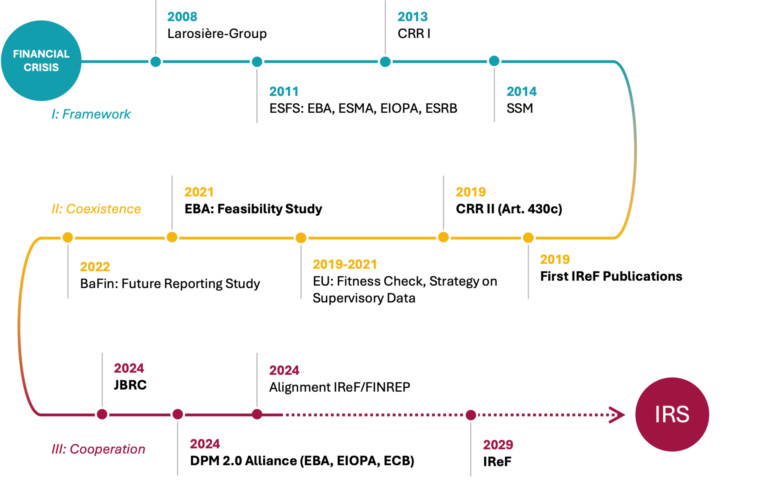

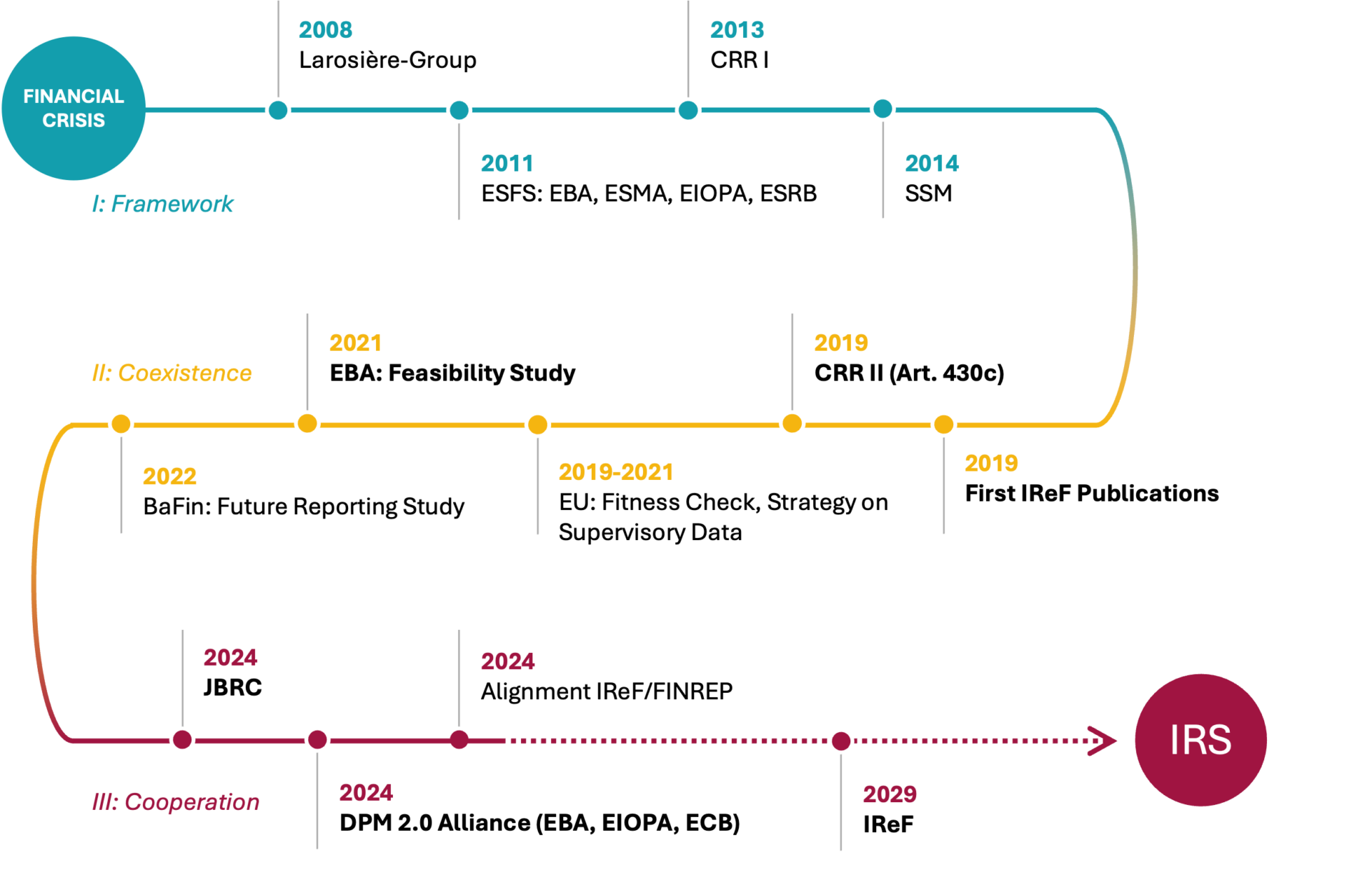

To better understand the evolution towards integrated reporting, it is helpful to revisit the key milestones since the financial crisis. In retrospect, three phases can be distinguished: the creation of a European supervisory framework (I), initial modernisation initiatives by individual stakeholders (II), and increasingly coordinated efforts toward an integrated target architecture (III).

Figure 1: The long road to reform towards an Integrated Reporting System (IRS)

I. The European Supervisory Framework

The 2008 financial crisis marked a turning point in banking supervision. It exposed the tight interconnectedness of financial markets and the inadequacy of national supervisory structures in a globalized world. These findings were confirmed by the Larosière-Group established by the EU and formed the basis for a comprehensive redesign of European financial supervision.

With the establishment of the European System of Financial Supervision (ESFS) in 2011, three sector‑specific authorities (EBA, ESMA and EIOPA) as well as the the European Systemic Risk Board (ESRB) were created. In addition, the ECB was appointed as the central supervisory authority, and the Single Supervisory Mechanism (SSM) began operations in 2014.

In addition, legislative reforms were supposed to create ‘level playing field’ for market participants. Whereas the Basel accords had previously been implemented via EU directives (CRD I–III), the EU introduced the Capital Requirements Regulation (CRR I) in 2013 as the first directly applicable regulation—reducing national room for maneuver and limiting supervisory arbitrage.

The European supervisory framework was thus established and, despite numerous changes since its inception, continues to shape the landscape of banking supervision. However, harmonizing legal frameworks and institutions at the EU level has not always been smooth, leading to increasing criticism in subsequent years.

II. Coexistence of Modernization Initiatives

The list of problems was long and included, among other things, a lack of cross-domain definitions, insufficient data exchange between authorities, duplicate reporting requirements and short-notice regulatory changes. All of this essentially reflects the opposite of what an IRS should be capable of in the future.

In the following years, multiple stakeholders therefore launched their own initiatives to modernise the reporting system. Particularly noteworthy are the EBA’s feasibility study and the ECB’s IReF programme.

The ECB faces substantial fragmentation in statistical reporting across the euro area. This is largely due to the fact that ECB requirements were historically interpreted and implemented differently by national central banks, often because additional data was needed for local purposes. For example, Germany uses the BISTA framework to meet the ECB’s Balance Sheet Items (BSI) reporting requirements, whereas Austria uses its monetary statistics. This complicates operations for internationally active banks and hinders progress toward an integrated European capital markets union.

With IReF, the ECB aims to systematically reduce this fragmentation and harmonise statistical reporting. For banks, this means a standardisation of requirements, but also a significant change in existing reporting architectures. The initial scope includes:

- Balance Sheet Items (BSI)

- Monetary Interest Rates Statistics (MIR)

- Securities Holdings Statistics (SHS-S)

- AnaCredit

These datasets are expected to be consolidated into a single EU regulation, with a draft anticipated by mid‑2026.

While the ECB focuses on statistical reporting with IReF, the EBA’s feasibility study covers the entire regulatory reporting system. The study was mandated by Article 430c of the 2019 CRR amendment, requiring an assessment of the conditions for an integrated reporting system.

The study’s conclusions broadly align with the key IRS characteristics and other contemporary initiatives (e.g., the EU Supervisory Data Strategy). However, the EBA places particular emphasis on the creation of common data dictionary (define once) and a common collection system (report once).

Despite considerable overlap between these initiatives, their concrete implementation requires much closer cooperation between all parties involved. Even if the ECB initially concentrates on statistical reporting, the downstream implications of IReF must be considered in the context of an IRS.

Otherwise, isolated design choices could create technical or functional path dependencies that complicate future integration of prudential and resolution reporting. To avoid this, IRS synergies should be embedded in IReF from the outset.

III. Cooperation between stakeholders with regard to an IRS

Against this backdrop, coordination between the institutions involved is becoming increasingly important. In organisational terms, this is reflected in the establishment of the Joint Bank Reporting Committee (JBRC), which serves as a platform for exchange between supervisors, legislators and – via a dedicated subgroup– the industry.

One of its key responsibilities is the development of a cross-domain common data dictionary as the foundation for semantic integration of regulatory reporting.

On the technical side, DPM 2.0 (DPM Refit) plays a central role. The EBA’s Data Point Model forms the semantic backbone of prudential reporting frameworks such as COREP and FINREP.

DPM 2.0 is a technical enhancement of this toolkit. In addition to improvements in data modelling and validation, it also coincides with the switch to the new CSV format for reporting submissions. This format significantly reduces file sizes, thereby facilitating the processing of the high data volumes expected under IReF in the future.

Crucially for the IRS target picture, the ECB will describe all IReF requirements based on DPM 2.0. This will create a common technical standard that will greatly facilitate the subsequent integration of further reporting domains by the EBA.

Another example of the increasing alignment is the discussion about the possible integration of FINREP (Solo) into the emerging IReF data model. While no final decision has been made, the debate illustrates the strategic direction and growing cooperation between the institutions.

Conclusion

The development towards an integrated reporting system is not a short-term undertaking, but rather a gradual process of change spanning several decades.

IReF represents an important milestone in this process, addressing initial design shortcomings in European supervision: it harmonises statistical reporting, sets new technical standards and strengthens institutional cooperation. At the same time, many current initiatives already contribute to the broader IRS vision.

For banks this means that those who understand where regulatory reporting is heading can not only meet requirements more efficiently but also leverage them strategically to build a future‑proof data and reporting architecture.

IReF Community – stay up to date with all the latest developments

In our IReF community, we regularly inform you about news, drafts and implementation experiences.