Property value drives sustainable growth

CRR III has been in force for more than a year now. And yet many institutions are still not fully exploiting the potential of the new regulations. With the introduction of ‘property values’, a new framework concept for the valuation of real estate collateral has been implemented. This offers potential savings in risk-weighted assets, particularly for institutions with a high volume of real estate loans. The equity capital that is freed up opens up growth opportunities and advantages in pricing. It also makes it easier to meet the reporting requirements of WIFSTA. Due to the existing transition periods, it is highly recommended that institutions address their specific potential in a timely manner.

Included in this collection:

Open collection

Why Europe’s banks need to reassess geopolitical risks

Bundesbank’s Targeted Review of the design of lending guidelines in the LSI environment

AMLR Redefines Risk Analysis: Moving Beyond a Checkbox Exercise – Why Regulators Are Rethinking Their Approach

9th Amendment to the MaRisk 2026: What reliefs does the consultation offer to small and very small institutions (SNCIs)?

Instant Payments Regulation: Implementing Reporting Requirements Efficiently – Excel Upload or an Integrated Reporting Solution?

Preferential Treatment of Retail Exposures in the Credit Risk Standardised Approach (CRSA) – EBA clarifies requirements regarding the granularity criterion

Artificial Intelligence in Treasury – from periodic financial reporting to a continuous management function

Changes to the LSI Stress Test 2026

CRR III and the property business: Removing the brake on new business

Early repayment penalty: Are liquidity costs the same as counterparty risk costs?1

Regulatory principles in accordance with CRR III

Due to the extensive nature of the changes, the redesign of the framework for assessing real estate collateral in Article 229 CRR has not yet been widely adopted in institutional practice. The concept of ‘property value’, i.e. sustainable real estate value, has been adopted from the Basel III proposals:

Art. 229 (1) CRR III

b) the value is estimated using prudent conservative valuation criteria that meet all of the following requirements:

(i) expected price increases are not included in the value;

(ii) the value is adjusted to take into account the possibility that the current market value may be significantly higher than the value that could be sustainably achieved over the term of the loan

In addition, the valuation is carried out by an independent expert, including clear and transparent documentation. Furthermore, the property value may not exceed the market value of the property.

This has been binding for new business since 1 January 2025. The handling of existing business must be regulated by the end of 2027.

CRR III – 360° View

The changes to CRR III affect all credit institutions and all types of risk and have a far-reaching impact on overall bank management. We present the key adjustments and areas where action is needed.

European and national implementation

The European Central Bank (ECB) commented on the new value concept in its Supervision Newsletter dated 14 August 2024. In it, it highlights the need for cautious and conservative valuation of real estate collateral and emphasises the need to continuously monitor value development on the basis of market data.

This is also addressed in Article 208(3) CRR, according to which credit institutions must monitor market fluctuations in property values in order to identify significant losses in value and the need to adjust the value of collateral.

The national banking supervisory authority has stated that there are two possible approaches to operationalising ‘property value’ in Germany, see vdp presentation: Property value in accordance with Article 229 (1) CRR III – vdp – Association of German Pfandbrief Banks

- The mortgage lending value in accordance with Section 16 (2) sentences 1 to 3 of the German Pfandbrief Act (PfandBG) in conjunction with the BelWertV (Mortgage Lending Value Regulation) fulfils the requirements of Article 229 (1) CRR in all cases.

- Alternatively, market value can be used as a basis. In a step following the market value determination, this value must be reviewed to determine whether an adjustment is necessary to meet the requirements of Art. 229 (1) letter b) CRR III. While the market value is determined on an object-specific basis, this review and, if necessary, adjustment of the market value can be carried out on a portfolio-specific basis based on statistical evaluations of relevant market data.

The new value concept therefore does not represent a completely new calculation logic, but rather provides the framework for a methodology that combines individual market value with consistent market data analysis:

Property value = market value – appropriate deduction.

Compared to the mortgage lending value, this results in potential. In the event of significant market fluctuations, the property value must be reviewed. In summary:

Methodology of vdp and vdpResearch

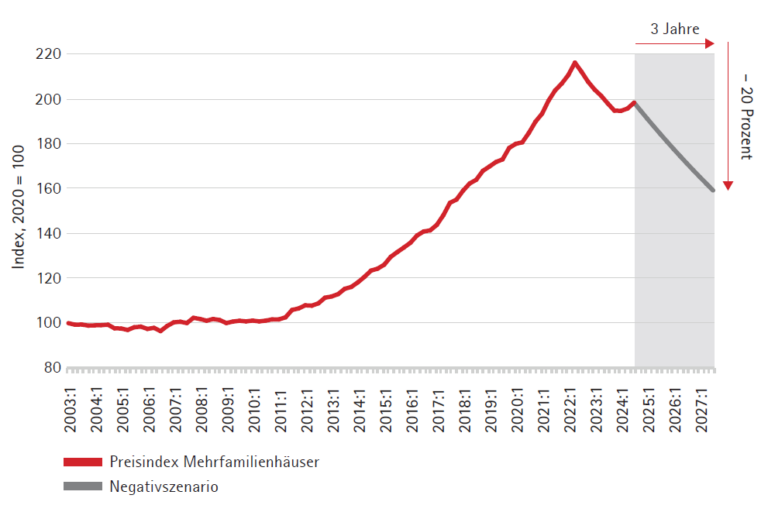

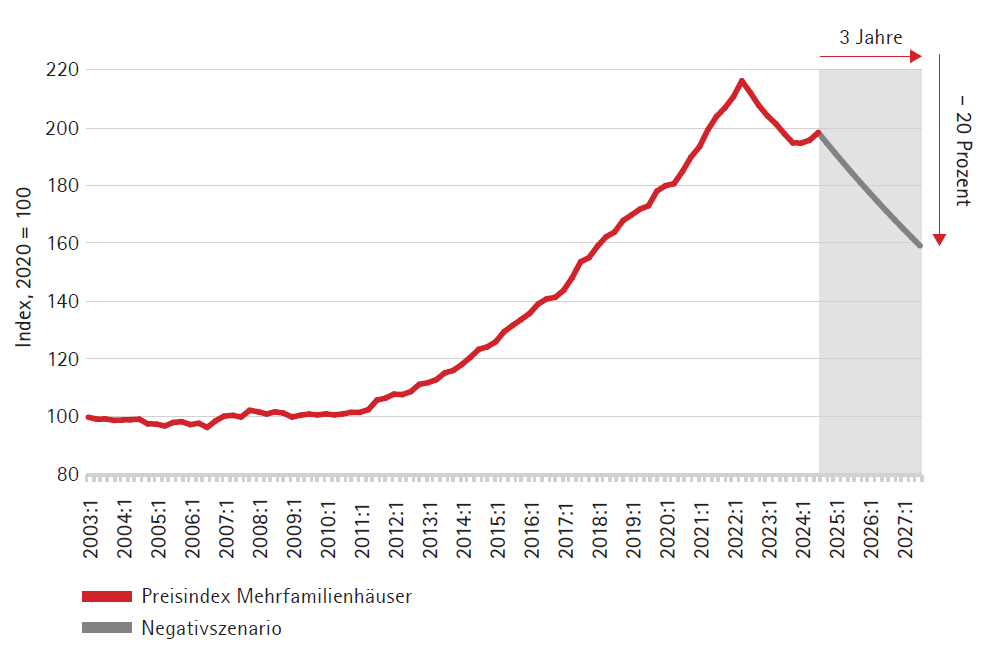

The vdp and vdpResearch GmbH have developed a discount method that enables the application of a market data-based discount to the individual market value of a property. For different types of properties, such as condominiums or office buildings, quarterly discounts can be obtained that are based on current market developments.

When deriving the discounts, the basic idea is to break down the property time series into a trend and a cyclical component in order to filter out cyclical fluctuations. In addition, a conservative buffer in the form of a hypothetical decline in market value is already taken into account when deriving the parameters to ensure that, in the event of a real decline in market value, the vdp discount remains valid as long as there is no distinct market crisis.

Figure 1: Market price time series with negative scenario (source: vdpResearch1)

Benefit analysis of property value

1. Individual loan perspective:

The advantages of property value are illustrated below using the example of a loan for a single-family home. The following framework applies:

| Input | Value |

| Exposure TEUR | 500 |

| Property value TEUR | 625 |

| Mortgage lending value in % | 75 % |

| Property value in % | 90 % |

| Typ property | Living |

| Typ dept | Retail |

| RW secured | 20 % |

| RW unsecured | 75 % |

Table 1: Sample calculation of property value for an individual loan

We expect a 10 % discount on the property value, which is a conservative estimate in the current market phase and would withstand a significant market downturn of over 20% based on the vdp methodology.

In the standardised approach to credit risk, the secured portion of the claim is assigned a risk weight of 20 %, while the unsecured portion is assigned a risk weight of 75 %. 55 % of the collateral value can be recognised as the secured portion. If the different collateral values are taken into account, the mortgage lending value results in a privileged volume of € 257.8 thousand, while the property value results in € 309.4 thousand. If the risk weight is now calculated by combining the secured and unsecured portions, the result is approximately 46.6 % for the mortgage lending value and 41.0 % for the property value. This means that in this specific case, approximately € 28.4 thousand in RWA savings can be achieved.

Further aspects:

- When granting large property-backed loans in the corporate receivables class, the savings potential increases because the unsecured portion is assigned a risk weight of 100 %.

- Commercial property offers lower savings potential than residential property, as the secured portion may only be weighted at 60 % risk. Nevertheless, switching to property value can still be worthwhile in this case.

- In the context of WIFSTA reports, BaFin criticises the continuing very conservative approach in Germany. The exclusive use of the mortgage lending value often leads to economically implausibly low values. In view of this, too, the use of the new European standard is an obvious choice.

2. Portfolio view

As expected, the savings potential in relation to the overall portfolio view depends considerably on the portfolio structure and is higher the more real estate-backed positions there are in the portfolio. In addition, the structure within the real estate-backed portfolio plays a decisive role. Our analyses show that for a bank with approximately 25% exposure to real estate-backed positions, RWA savings at the overall portfolio level of around 5 % are realistic. This assumes that the original retail and corporate exposure classes occur with approximately the same frequency in the property-backed business and that the discount on the property value compared to the mortgage lending value is as shown above.

A precise analysis based on the specific portfolio structure can be determined using the specially developed msg RWA Analyzer.

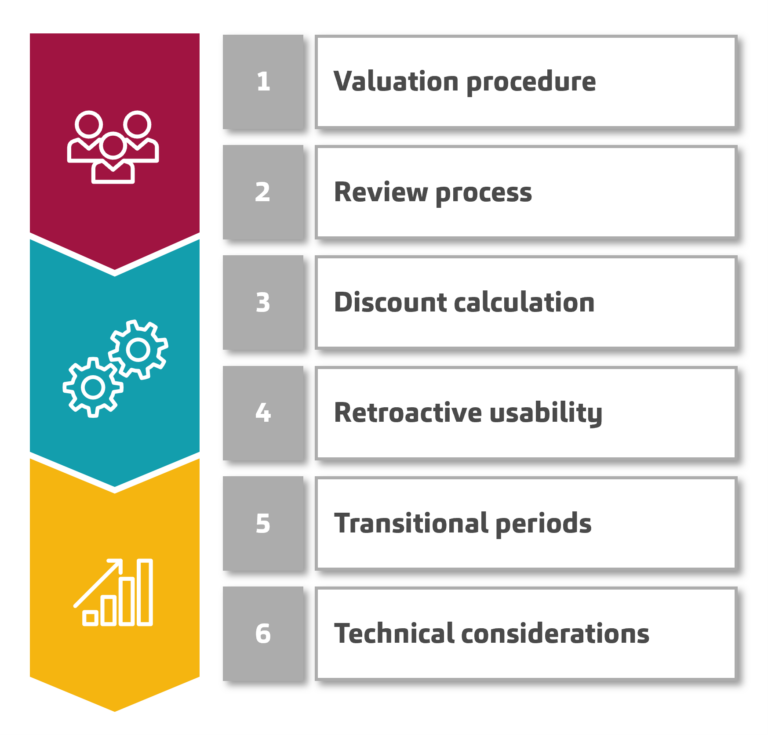

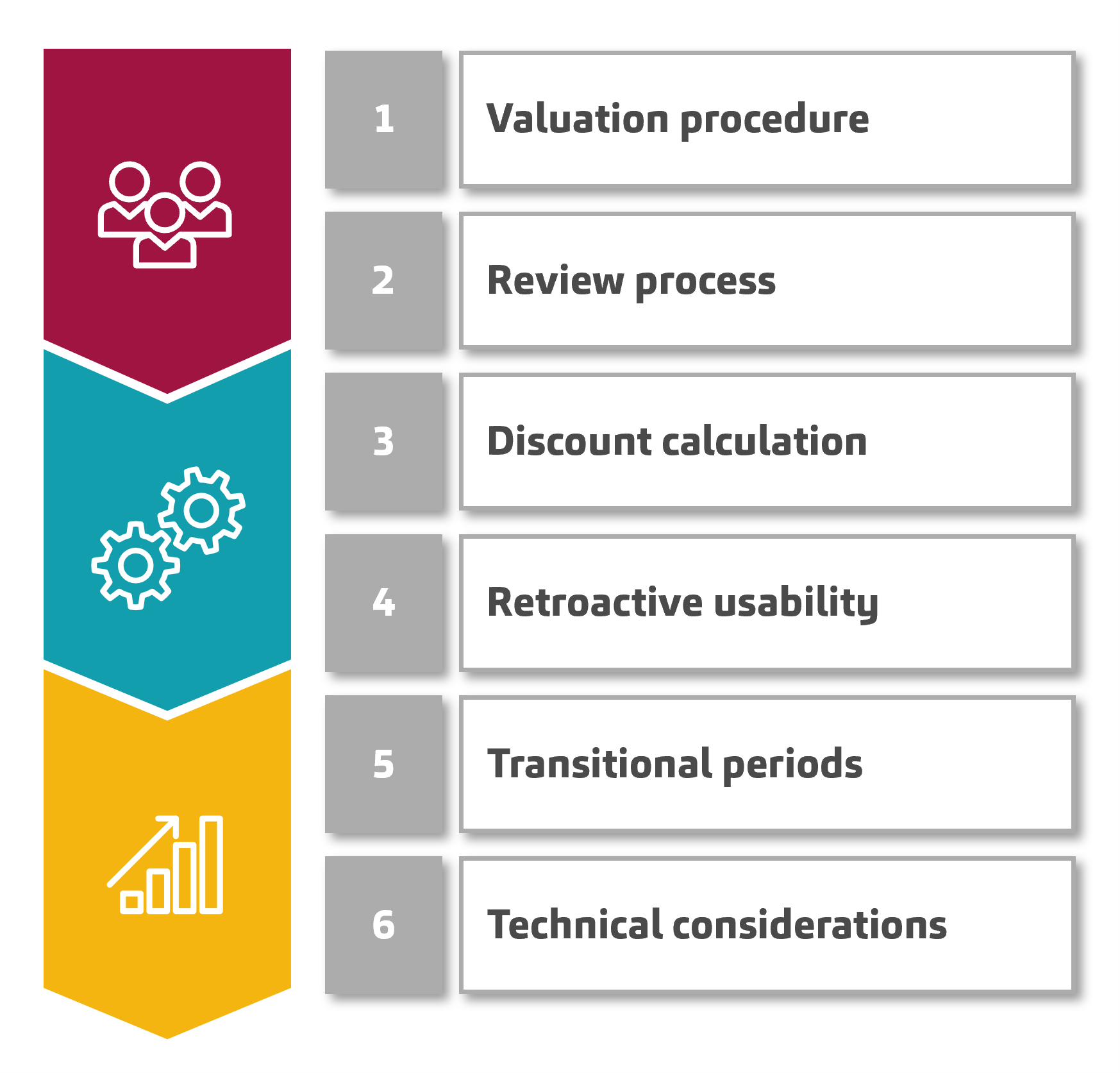

Implementation in banks

Figure 2: Key elements for successful implementation in banks

- Valuation procedure:

The new valuation procedure must be introduced in a structured manner. Prior to introduction, the discount logic for the property value must be documented and validated regularly in the future. The model must be understood and reviewed within the institution. - Review process:

The review process for the (respective) collateral value must be adjusted and the conditions for revaluations must be taken into account. A distinction must continue to be made between monitoring at portfolio and individual level and adjustment at individual level.

- Discount calculation:

When using vdp discounts, the relevant discount must be applied to determine the property value, depending on the property segment and date of valuation. It is advisable to specify a fallback. - Retroactive usability:

The retroactive usability of the property value must be checked on the basis of data quality analyses. The type and quality of the property valuation reports, the quality of the data stored in the security system and the review process in accordance with Art. 208 CRR III with regard to the past play a role here. - Transitional periods:

For existing business (until 2024), the transition to property value can be completed by 31 December 2027. For privileged new business from 1 January 2025, the valuation method chosen for the first application is binding, i.e. if the mortgage lending value is used, no change is possible. - Technical consideration:

The process for taking vdp discounts into account must be defined and their use in regulatory reporting ensured. In savings banks, largely automated system-based use is already possible.

We would be happy to support you in your project. Our free online sessions provide you with a concise overview of the transition to property value and show you how to carry out the pre-check and implementation efficiently and smoothly.

When?

Conclusion

Property value offers institutions with large portfolios of real estate collateral in particular the opportunity to achieve significant RWA savings. This improves the usability of scarce equity capital, resulting in growth and earnings potential. The reduction in capital tied up opens up new pricing scope in new business, which can be used to expand market position and increase margins.

Due to the existing transitional arrangements, it is advisable to address this issue promptly, as the savings potential decreases with each passing day and will be completely lost by the end of 2027 at the latest. Conversely, the current situation offers all institutions the opportunity to benefit in the long term and position themselves successfully in the competitive environment by taking decisive and orderly action.